|

|

| NOMINATE NOW | |

Dear Industry Leader,

The Next Capital of People Excellence is Here.

We are delighted to announce the launch of the 6th Edition of The Economic Times Human Capital Awards (ETHCA) 2027 , recognising organisations that are creating exceptional workplaces, developing future-ready talent, and redefining the future of work.

Date: February 26, 2027

11 HR Pillars.

From Talent Acquisition and Learning & Development to Leadership & Talent Management, Employee Experience & Engagement, HR Technology & AI, Compensation & Benefits, Rewards & Recognition, Compliance, Governance & Legal, and Sustainability & Social Impact, ETHCA celebrates excellence across the entire HR ecosystem.

Nominations are officially open.

Grab the Super Launch Advantage valid until August 24, 2026. ..

Showcase your people initiatives. Gain the recognition your organisation deserves.

Take the next step. Submit your nominations.

Warm regards,

Because the future is shaped by organisations that invest in their people. |

|

| NOMINATE NOW | |

|

|

|

Monday, 10 August 2026

Watch This Space: ETHCA 2027 Is Here

ETHRWorld's August special | AI-linked hiring in India outpaces job losses by over 51,000 | US proposes to end the 60-day H-1B grace period

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Latest Releases from PIB

Sunday, 9 August 2026

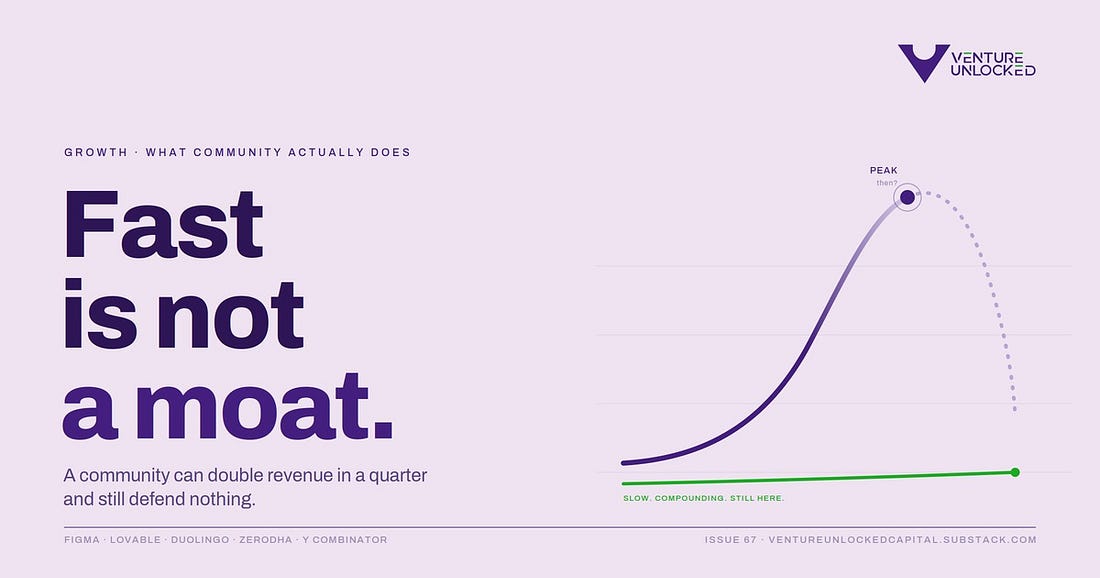

Fast Is Not a Moat

Fast Is Not a MoatIssue 67 : Community can double your revenue in a quarter and still defend nothing. How to tell the difference.

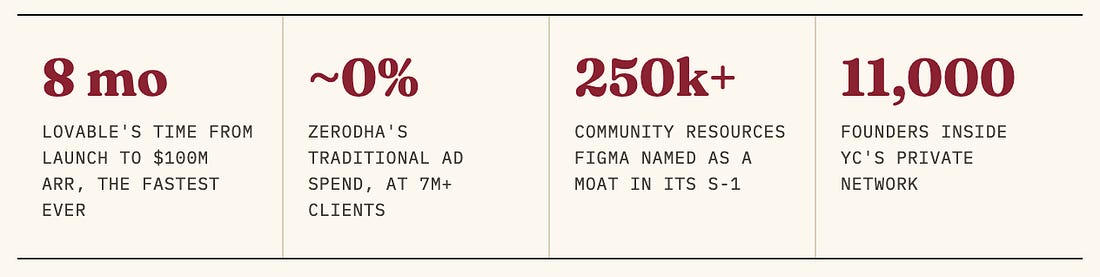

In late 2024, Lovable was a beta product with a community of about ten thousand people. Eight months after its commercial launch, it crossed $100 million in annual recurring revenue, the fastest any software company has ever reached that mark, faster than OpenAI, faster than Cursor, with a team of roughly forty five people. By November 2025 it had doubled again to $200 million. Almost every account of that run uses the same word to explain it. Community. A hundred-thousand-strong Discord, users sharing apps they had built, word of mouth compounding daily. And it is true. Community was the engine.

But here is the number that sits awkwardly next to the triumph. In the summer of 2025, Barclays found that traffic to Lovable had fallen about 40% from its peak, even as paying revenue kept doubling. So the community brought the world to the door at a speed no company had matched, and then a large part of it wandered off, while the people who paid stayed for the product. Which raises the question this issue is about. Was that community a moat, or just a very fast channel? You cannot answer that until you accept that community is not one thing.

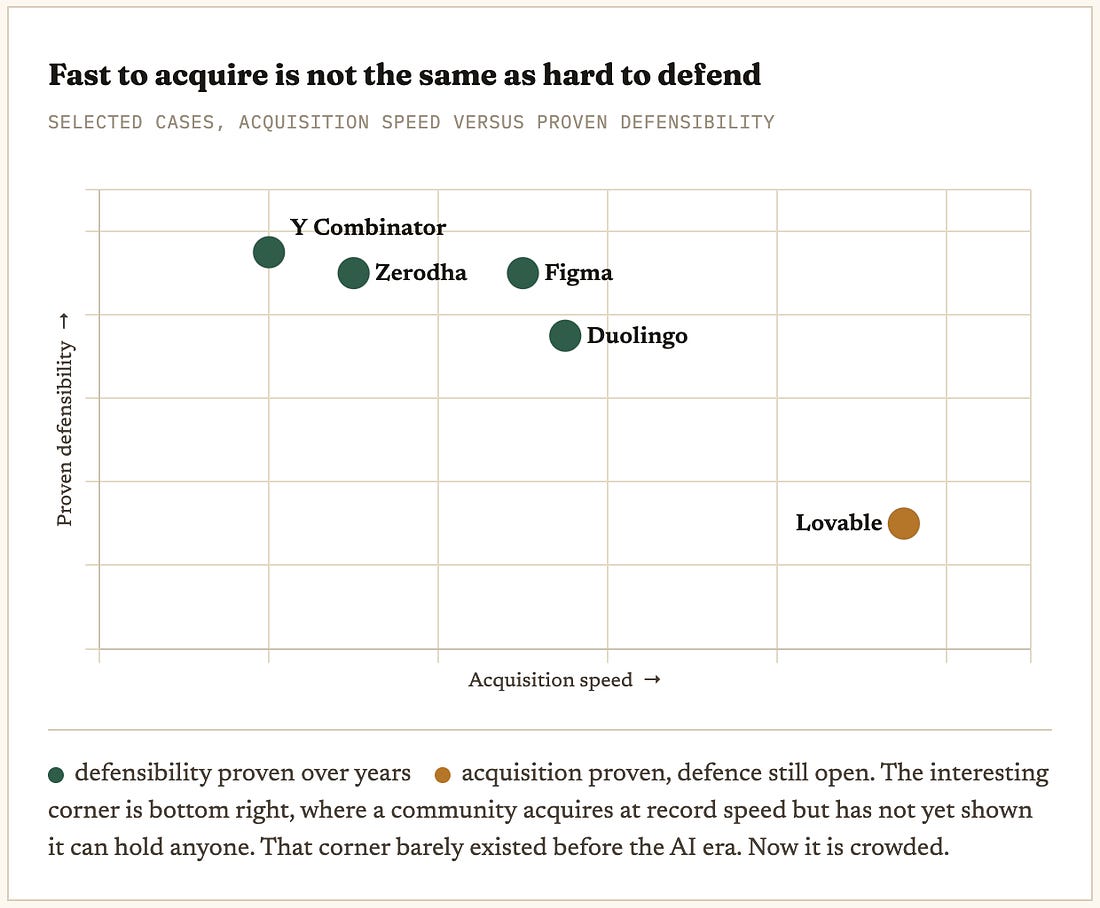

Section oneThe word hides three jobsWhen founders and investors say community, they usually mean one of three jobs, and they are not interchangeable. Each costs a different amount, each is defended differently, and each has its own failure mode. The first job is to acquire. Community as a distribution channel, lowering the cost of getting users in the door. The second is to retain. Community as the reason people stay, the network that makes leaving feel like a loss. The third is to defend. Community as a structural moat, where the accumulated behaviour of members makes the product genuinely hard for a competitor to replicate at any price.

These three jobs sit on a gradient of cost and defensibility. Acquisition is the cheapest to start and the easiest to copy. Defence is the most expensive to build and nearly impossible to replicate. Retention is the transition zone between them. Plot the well-known cases on that gradient and the picture gets clarifying.

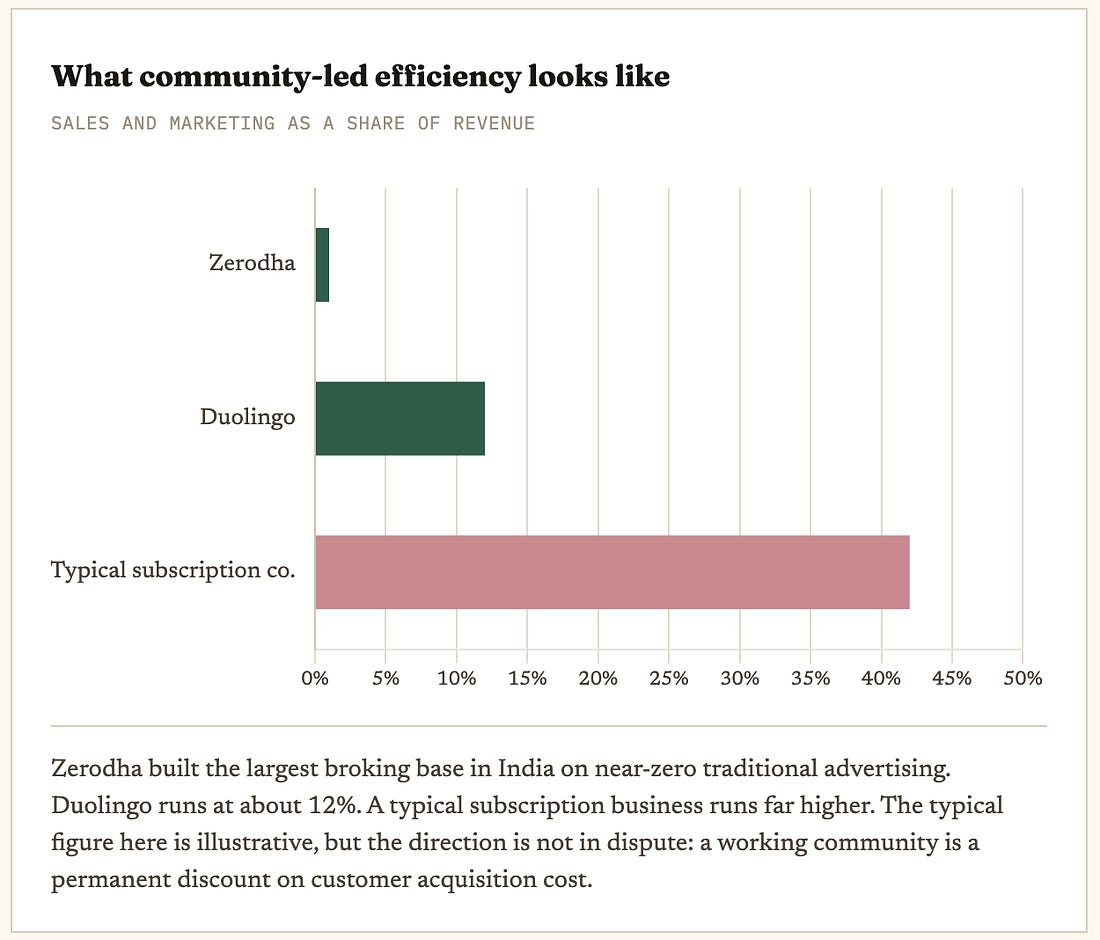

Section twoWhat defence actually costs: FigmaWhen Figma filed to go public, its community was not a line in the marketing section. It was described in the S-1 as a platform moat. More than 250,000 community resources, over 10,000 plugins built by users, hundreds of local chapters and design events. None of that is a by-product. Each piece was resourced, owned and given years to compound. That is what a defence-grade community looks like, and it is worth being honest about the price. It is slow, it is deliberate, and it is expensive. Figma did not stumble into a moat. It funded one for a decade and then told its regulators, in writing, that the money had bought defensibility. Hold that standard next to the industry baseline. In one 2025 survey of community professionals, 30% were solo operators and 17% had no full-time community staff at all, the highest figure ever recorded. Most companies that claim a community moat are spending acquisition money on it. Figma spent defence money. That gap is the whole story of why most community moats never materialise. Section threeThe case that put a number on it: DuolingoDuolingo is useful because it ran the experiment most companies never do. It measured what its community was worth, and then it turned the tap down and watched what happened. For years Duolingo grew with almost no paid media. It spent about $90.5 million on sales and marketing in 2024, roughly 12% of its $748 million in revenue, a fraction of what comparable subscription companies spend. The product and the social engine did the acquiring, and the member-to-member energy, forums, shared streaks, leaderboards, did the retaining. Its chief marketing officer describes the daily social presence not as an acquisition tactic but as a retention driver. Then in 2025 the company deliberately dialled back the irreverent content that had made it famous, and it told shareholders, in filed documents, that doing so measurably slowed user growth. That is a rare and valuable admission. A public company putting a number on the value of what most decks wave away as vibes, and proving it by removing it. The lesson is not that community works. It is more precise than that. Duolingo shows community doing the retain job, verifiably, and shows that the job is real enough that switching it off costs you. That is a different and stronger claim than Lovable’s, where the acquire job was spectacular and the retain job is still unproven.

Section fourThe Indian moat nobody paid for: ZerodhaThe cleanest community moat in India was built without a marketing budget. Zerodha became the country’s largest broker, with roughly 7.26 million active clients and around 15 to 16% market share by 2025, in an industry where rivals spend heavily on television and sponsorships. Zerodha spent almost nothing on traditional advertising. What it built instead was a trust engine. Varsity, a free and genuinely deep stock-market education library, and TradingQ&A, an active forum where investors answered each other. In a market where retail investors were wary of a discount broker with no research arm, the community solved the trust problem that advertising could not have bought at any price. Run Zerodha through the three jobs and you see the full gradient inside one company. Varsity started as acquisition, educate a confused first-time investor and they open an account. It became retention, the ecosystem kept teaching them so they stayed. And it hardened into defence, because a decade of free content and an active peer forum is now something a competitor cannot cheaply replicate. It is the Indian Figma, a community that became a structural moat, except Zerodha built it while bootstrapped. There is a small, telling coda for the investors reading this. GrowthX, founded by operators who had led growth at CRED and Razorpay, began life as a community and turned into a paid education business, and it has since partnered with Zerodha. Community as a channel, growing up into community as a business model, inside the same ecosystem. Section fiveWhen community is the product: Y CombinatorThe last case is the one where community stops being an asset around the product and becomes the product itself. Ask most YC founders what the $500,000 cheque actually buys and they will tell you the money is not the point. The network is. That network runs on Bookface, YC’s private forum connecting more than 11,000 founders across nearly 5,700 companies. Founders answer each other’s questions, make introductions, and sell each other their first contracts. YC-backed companies raise their next round faster and at higher valuations, in part because the community vouches for them. The accelerator’s real product is membership in that room. It is also the hardest of the five to copy, and the clearest proof that community can be a moat and a business model at once. But note the vintage. YC has been compounding this for twenty years, and even it now faces the question of whether four batches a year dilutes the very network that is the product. Defence-grade community is not just expensive. It is slow in a way that runs against every incentive a young company has. Our readPut the five cases in a line and the argument makes itself. Figma, Zerodha and YC are the answered cases, communities that became genuine moats, and every one of them took the better part of a decade and was funded as infrastructure rather than run as a campaign. Duolingo is the measured case, community proven to do the retain job because turning it off cost real growth. Lovable is the open case, the acquire job done at a speed nobody has ever matched, with the retain and defend jobs still unproven. The AI era has not made community more powerful. It has made one specific job, acquisition, breathtakingly fast, while leaving the other two exactly as slow and expensive as they always were. The danger is reading a fast-acquiring community as a durable one. A hundred-thousand-person Discord that doubles your revenue in a quarter is a channel until proven otherwise, and the proof takes years, not quarters. For India specifically this matters more, not less. Where trust is scarce and paid acquisition is expensive relative to what a customer is worth, a community that compounds down your acquisition cost is worth more here than the global playbooks assume. But only for founders patient enough to fund it like Zerodha funded Varsity, as a ten-year asset, rather than as this quarter’s growth hack. Section sixWhat is actually open for Indian founders and investorsIf the analysis is right, it points at specific, unbuilt opportunities. Four of them look genuinely open.

Over the last three issues we have watched capital get harder to raise and harder to exit. Community is the one asset that runs the other way. It gets cheaper to maintain and harder to copy the longer you hold it, which makes it the rare moat a capital-starved market is actually well suited to build. The catch is that it pays out on a timeline that fights every quarterly instinct a founder has. The one questionBefore you call a community a moat, ask which of the three jobs it is actually doing. Acquiring is cheap and copyable. Defending is expensive and rare. Most communities are doing the first while being valued as if they did the third. Speed is not durability. Lovable acquired faster than any company in history and still may turn out to have built a channel, not a moat. Figma, Zerodha and YC took a decade each. If you want the moat, fund it like the ones that got it, and give it the years the cheap version never needs. A note on the numbers. Lovable’s ARR and headcount are company-reported and widely cited; the 40% traffic decline is from Barclays research in mid-2025. Figma’s community figures are drawn from its S-1. Duolingo’s marketing spend and its shareholder disclosures on reduced social content are from its public filings. Zerodha is privately held, so its client count and near-zero ad spend are from reported estimates rather than audited disclosure. YC’s network figures are company-stated. Several community-impact statistics in this space originate with community-software vendors and should be treated as directional. Verify anything load-bearing before quoting. Thanks for reading. If a founder in your circle is about to pitch a Discord/Slack/WhatsApp as a moat, send them the one question first. Shubham Bopche - Editor Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|