Fintech, After the NoiseIssue 50 : What actually changed between 2021 and 2025 - and what India’s fintech ecosystem is quietly being asked to build next (2026)A note before we beginThis is the 50th issue of Venture Unlocked. And it’s arriving at a strange moment. In 2025, fintech funding in India didn’t collapse. Yet almost everything about how fintech is built, evaluated, and funded changed. Roughly $2.4 billion flowed into the sector - about the same as the year before - but it moved through a completely different filter: fewer rounds, slower diligence, and far less tolerance for fragility. If you were only watching headlines, it looked like a quiet year. If you were inside the system, it felt like a line had been crossed.

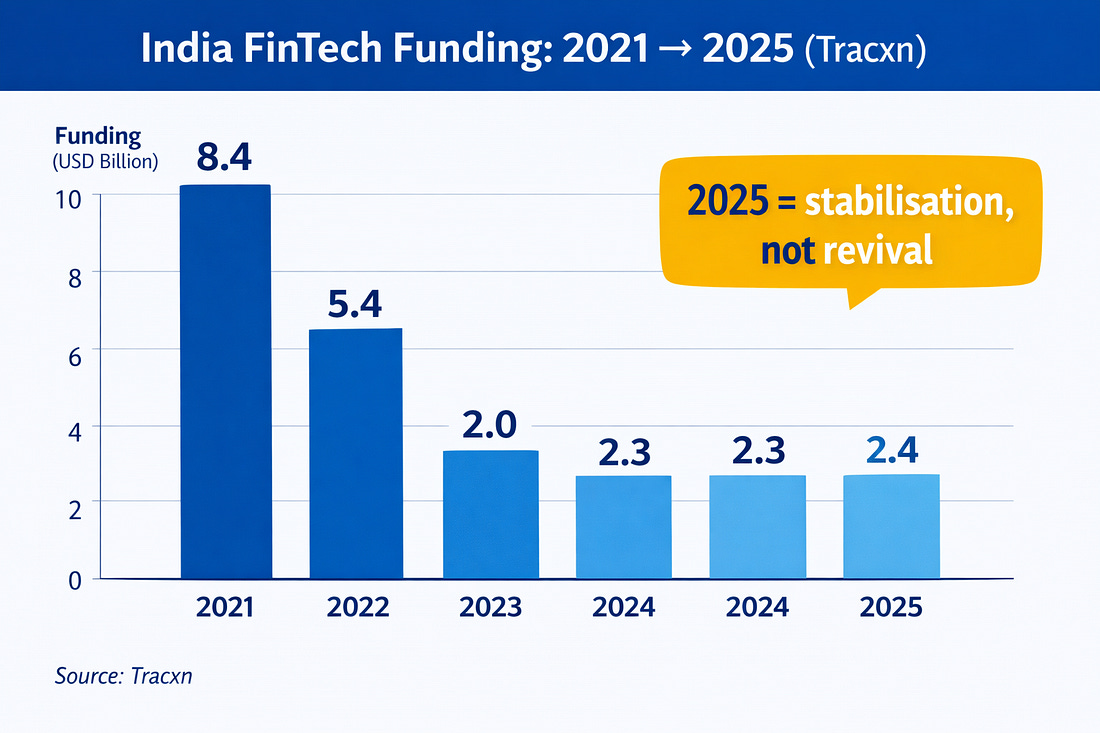

The funding numbers don’t tell the full story - but they matterLet’s begin with the data, without drama. India’s fintech sector raised roughly $2.4 billion in 2025, marginally higher than 2024 and far below the 2021 peak of $8.4 billion. On the surface, this looks like stagnation.

This wasn’t capital exiting fintech. It was capital recalibrating its expectations. The more revealing shift was where that capital went.

The market wasn’t contradicting itself. It was saying something very specific:

2021 rewarded velocity. That distinction underpins everything that follows. What quietly stopped working in fintechThe shift in fintech wasn’t triggered by a single failure. It happened through accumulated friction. Between 2022 and 2025, investors didn’t suddenly stop liking certain fintech models. The clearest evidence of this showed up at the earliest stages. As seed funding tightened, several patterns began to struggle under scrutiny:

This pressure didn’t always show up as public shutdowns. More often, it showed up as:

By ecosystem estimates, over 11,000 Indian startups shut down or went dormant across 2024–2025, many at early stages where access to fresh capital tightened fastest. What failed wasn’t demand. What failed was thin error tolerance. In a regime where capital is selective, models that depend on constant fundraising lose their margin for missteps. Fintech didn’t disappear - it moved deeper into the systemAs surface-level fintech models became harder to defend, capital didn’t leave the ecosystem. It repositioned itself. Between 2023 and 2025, the most consistent pattern across funded fintech companies was not the category they operated in, but where they sat in the financial stack. Investors became less interested in products that lived at the edge of the system - interfaces, acquisition layers, promotional rails - and more focused on companies embedded inside operational workflows. Diligence conversations changed. Instead of asking:

Investors increasingly asked:

These were not abstract questions. They reflected a broader recognition that in a regulated, capital-constrained environment, value accrues to systems financial institutions cannot easily do without. Infrastructure doesn’t win because it is exciting. Once a product touches underwriting logic, settlement flows, compliance trails, or treasury operations, it stops being optional. Removing it introduces risk. And risk - more than growth - is what capital became focused on pricing correctly in this cycle. Financial infrastructure emerged as the strongest investable categoryAcross Indian VCs (Elevation, Peak XV, Accel, Z47, Prime, Nexus) and global funds, one pattern became consistent: Capital flowed toward fintech companies that embedded themselves into the operating fabric of financial institutions. These were products sitting inside:

They were not loud companies. But they shared one important trait: They became hard to remove. Case study: Knight FinTechKnight did not pitch itself as a lender or marketplace. It positioned itself as an operating layer for collaborative lending, covering underwriting, orchestration, monitoring, and compliance. That framing resonated. The result was a $23.6 million Series A, led by Accel with participation from Prime Venture Partners and 3one4 Capital. What investors were underwriting was not short-term growth. Infrastructure doesn’t trend. Regulation stopped being a constraint - and became product surfaceAnother major shift became visible through 2024 and 2025. Regulation stopped being something teams “Handled later”. With the Digital Personal Data Protection Act (DPDP) in India, along with tightening AML and data regulations globally, compliance moved from the back office to core system design. This created a new class of fintech opportunity: These products enable:

They don’t sell aspiration. They sell certainty. Case study: Data SutramData Sutram operates at the intersection of fraud intelligence, risk monitoring, and compliance. Its customers are regulated institutions. Its value proposition is not growth acceleration, but risk reduction. This is precisely why such platforms continued to attract backing even as consumer fintech cooled. Consent Management Systems quietly became an emerging marketOne of the most India-specific structural changes of this cycle didn’t come from venture capital. It came from law. With DPDP, consent stopped being:

And became:

Under DPDP, organisations must now:

This cannot be handled with documents or spreadsheets. It requires infrastructure. Why Consent Management Systems (CMS) emergedConsent Management Systems are no longer “privacy features”. They are:

For fintech, CMS sits at the intersection of:

Especially in India - where Account Aggregators normalised consent-led data sharing and DPDP formalised obligations - CMS became the control plane for data usage. From a VC lens, CMS has rare characteristics:

This is not just RegTech. It is data infrastructure. AI entered fintech - and the bar moved from “assist” to “decide”By 2025, nearly every fintech pitch mentioned AI. Very few received funding because of it. The shift was not about whether AI was present - but what role AI played inside the system. AI positioned as:

struggled to justify itself. AI that:

found traction. In Indian fintech, AI-led automation has been reported to reduce manual review effort by 30–50% in lending and risk workflows. That matters because AI that compresses cost-to-serve and improves risk outcomes directly improves unit economics. AI that merely explains decisions does not. Globally, this has been described as agentic finance. In India, it has appeared more quietly - embedded inside infrastructure. AI stopped being the headline. It became the machinery. Payments matured - and lost their glamourPayments never stopped growing. But their investability changed. Consumer-facing payment apps faced:

Capital instead moved toward:

Case study: JuspayJuspay raised $50 million in a WestBridge-led round, valuing it at $1.2 billion, becoming India’s first unicorn of 2026. Its strength was never visibility. It was reliability at scale. In fintech, invisibility is often strength. Wealth platforms followed a different trajectoryWealthtech survived the funding reset for a simple reason: Assets behave differently from users. Platforms focused on:

continued to find capital. Case study: AssetPlusAssetPlus scaled beyond ₹7,300 crore in AUM before raising ₹175 crore. The product wasn’t flashy. But the economics were undeniable. What capital stepped away from - quietly, consistentlyNo memo announced a retreat. But capital behaviour was clear. As seed-stage funding tightened, enthusiasm cooled for models that shared one or more of these traits:

Not because these ideas are invalid. But because their margin of error collapsed. Capital didn’t reject them. It prioritised fintech that could absorb stress without breaking. The pattern beneath it all: Dpeed is equals to DurabilityAcross all these shifts, one theme holds. Fintech stopped being about speed. It became about durability:

The companies that endured could answer one question clearly:

Irreversibility became the moat. Closing: What this 50th issue stands forVenture Unlocked began as a way to understand how funding works. Over time, it became something else. A way to notice small shifts before they become obvious. This issue exists because fintech crossed one of those quiet thresholds. Between 2021 and 2025, the ecosystem didn’t just go through a funding cycle. What emerged on the other side was not a new trend. It was a different standard. A standard where:

That is what connects infrastructure platforms, consent management systems, AI-led risk engines, payments rails, and wealth distribution layers. They are not exciting for the same reasons the last cycle’s fintech was. They are exciting because they last. This 50th issue is not a celebration. It is a marker. Of where fintech has arrived - Shubham Bopche Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Tuesday, 27 January 2026

Fintech, After the Noise

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment