The New Rule of EarlyStage AI FundraisingIssue 54 : How AI Capital Institutionalized, Faster Than Founders ExpectedIn early 2023, raising for an AI startup felt like catching a wave. When Midjourney spread organically through creative communities, the product felt magical. At that moment, the underwriting logic was simple:

Capital chased proximity to models, to talent, to narrative velocity.

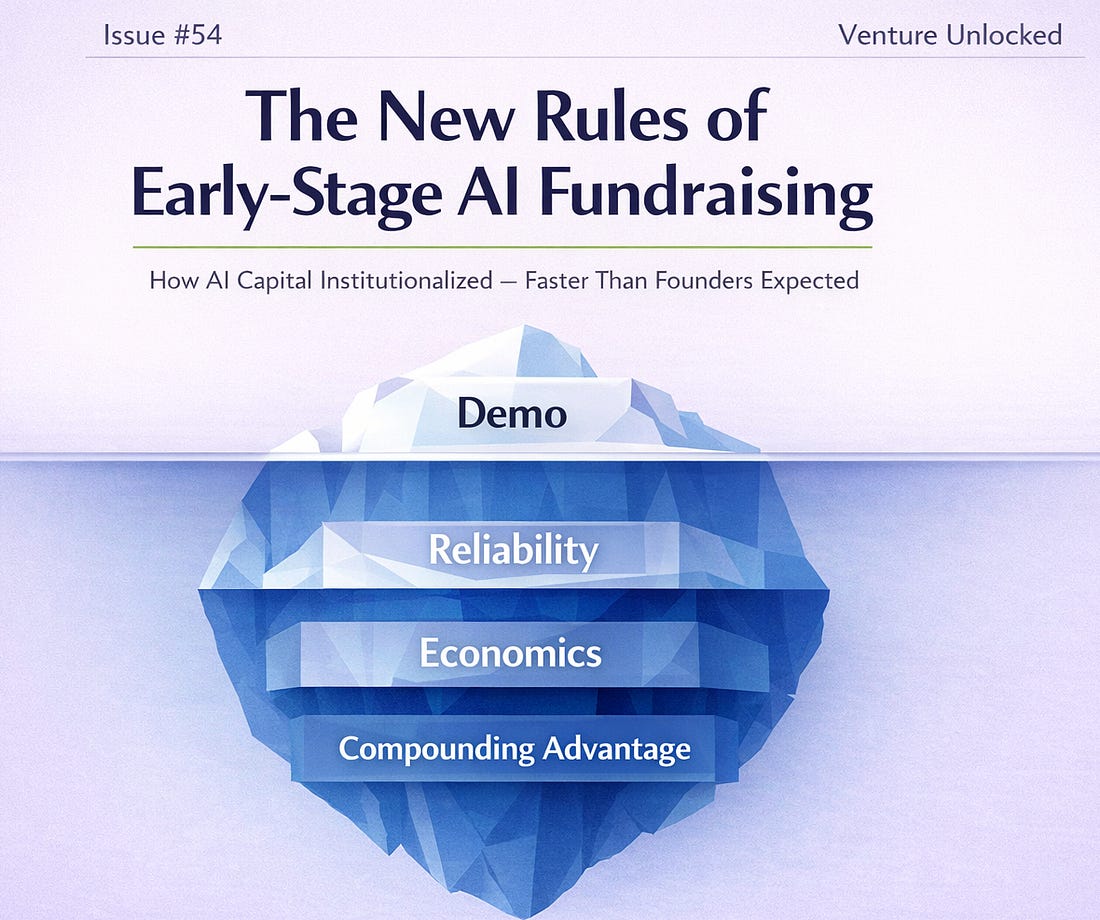

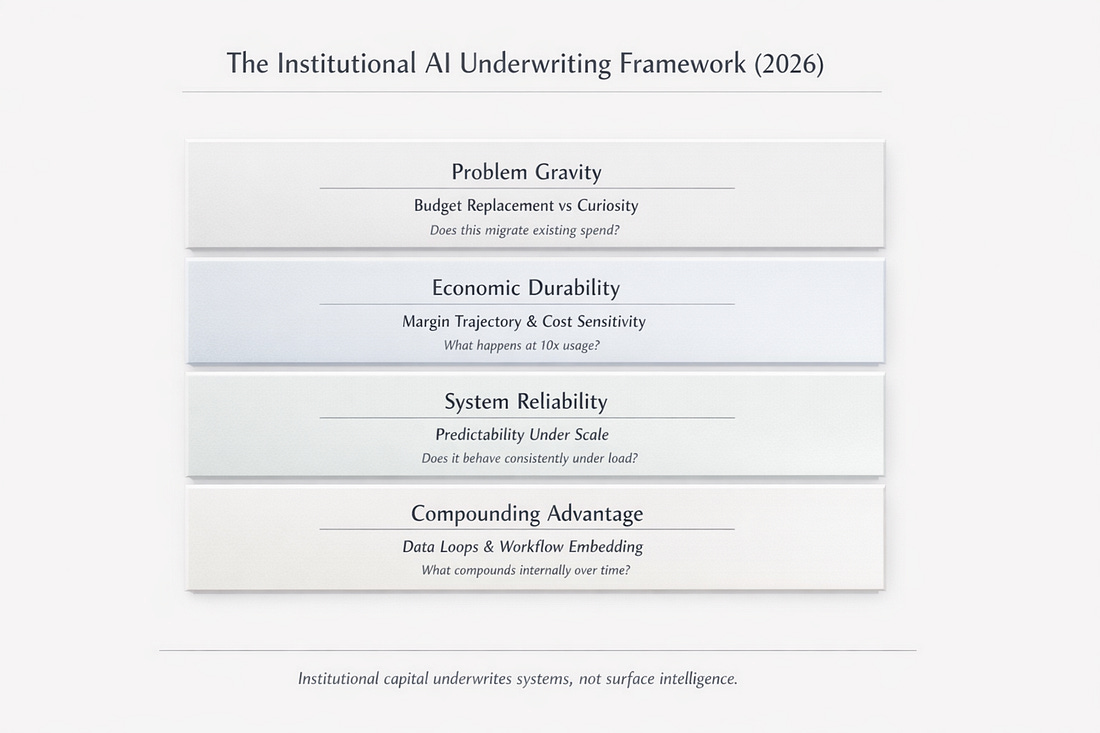

Before We Get to the Framework - A StoryA founder I spoke with recently closed a $4M seed in 2023 on a strong demo and a waitlist of 8,000 users. Eighteen months later, she was back in market for her Series A. Same product, meaningfully improved. Retention had held. Revenue had grown. She got passed on by eleven firms. Not because the business was broken. Because she walked in speaking 2023 language to 2026 investors. She led with excitement. They wanted to talk about gross margin architecture. That gap between how founders learned to pitch and how capital now listens - is what this piece is about. The Institutionalization Timeline of AI CapitalUnderstanding today’s fundraising climate requires understanding how quickly the capital stack evolved. Phase 1 - Narrative Capital (2023) This was the “access premium” era. Investors optimized for founders close to frontier models, teams with technical credibility, speed of iteration, and product demos that showed capability. Revenue quality mattered less. Unit economics mattered later. Distribution was assumed solvable. The bet was macro: if the platform shift is real, first movers win. Capital tolerated ambiguity because the category itself was expanding. Phase 2 — Saturation & Signal Compression (2024–2025) Then the wrapper explosion happened. Every workflow had an AI layer. Demos became sharper. Pitch decks became similar. User excitement became harder to interpret. The problem wasn’t innovation. It was signal noise. Capital learned three things quickly: model access was not defensible, surface-level AI was easily replicable, and early revenue did not always convert to embedded behavior. The market started asking harder questions: Is this workflow mission-critical? Does usage deepen over time? What happens if model providers improve tomorrow? Phase 3 — Institutional AI (2026) We are now in the third phase. Capital hasn’t disappeared. It has professionalized. According to PitchBook data, AI seed deal count grew significantly in 2023 but median seed valuations for AI-native companies compressed by late 2024, even as total dollars deployed increased. Capital didn’t retreat. It concentrated. The top quartile of AI seed rounds got larger. The middle compressed. That’s what institutionalization looks like in a funding table. Look at where large capital continues to flow: Databricks (data and infrastructure control), Scale AI (enterprise embedding), Anthropic (model-layer credibility). The pattern is consistent : infrastructure positioning, enterprise integration, margin visibility, control over critical components. The category shifted from novelty to systems. That shift redefined early-stage underwriting. What Institutional Capital Now UnderwritesThe biggest misunderstanding founders have today is this: they think AI got harder. It didn’t. It got more measurable. Institutional underwriting now revolves around four structural lenses. 1. Problem Gravity (Budget Replacement vs. Budget Creation) Walk into a Series A conversation today and describe your product as “AI-powered workflow automation.” Watch the room. The investors will nod politely and start probing for the thing underneath, where does it actually live in the customer’s stack? What breaks if they turn it off? Who owns the renewal decision? That’s what problem gravity actually means. Not a technical description. A gravity test. Does your product occupy a load-bearing position in someone’s operation or does it sit on the edge where a cancelled credit card ends the relationship? Capital prefers products that migrate existing spend because budget replacement signals inevitability. Curiosity-driven AI tools can grow quickly. Budget-replacing systems scale predictably. Institutional capital seeks inevitability, not enthusiasm. 2. Economic Durability (AI ≠ SaaS Economics) SaaS enjoyed structurally high and stable gross margins. AI introduces volatility: inference costs fluctuate, API pricing is external, power users distort cost curves, and usage growth increases compute dependency. Investors now ask at seed: What is your cost sensitivity? How does margin improve at 10x usage? What happens if API pricing shifts 20%? This is not skepticism. It’s risk modeling. SaaS took roughly a decade to develop standardized due diligence frameworks - CAC/LTV ratios, net revenue retention benchmarks, Rule of 40 conventions. These emerged organically through enough failed companies that investors could reverse-engineer what durability looked like. AI compressed that cycle violently. By late 2024, less than two years after ChatGPT normalized the category institutional investors were already asking AI founders about inference cost sensitivity and compliance readiness. Frameworks that took SaaS a decade to codify arrived in AI within 24 months. The founders who didn’t notice are the ones now struggling in diligence. 3. System Reliability (Capability vs. Predictability) Demos still matter. But capability is assumed. Institutional capital now evaluates failure tolerance, error handling, latency consistency, and compliance readiness. AI systems that work 80% of the time excite users. Institutional systems must work 99% of the time. That reliability gap defines the institutional round threshold. 4. Compounding Advantage (Moat Beyond the Model) The model layer evolves rapidly. If your defensibility depends solely on model performance, your durability depends on someone else’s roadmap. The capital prefers assets that compound internally: proprietary data loops, workflow embedding, integration depth, distribution leverage, ecosystem positioning. The moat has shifted upward from intelligence to integration.

Why Demos No Longer Anchor Institutional RoundsIn 2023, demos converted imagination into capital. In 2026, demos convert attention into diligence. The conversion event has moved. Today, investors probe: What percentage of users return weekly? What expands inside the account? Does usage correlate with measurable output? Do margins improve with retention? Consider Granola, the AI meeting notes tool which didn’t scale because transcription was accurate. It scaled because the output became the artifact teams actually used in follow-up emails, CRM updates, and project briefs. The AI wasn’t the product. The downstream workflow dependency was. That’s the difference between a feature and an embedded system.

How Institutional Capital Prices AI Risk - And What Traction Actually ProvesRevenue alone no longer signals readiness. That’s the uncomfortable truth for founders who closed pilots in 2023 and assumed they’d built a business. Institutional investors now run two parallel tracks in diligence: Track 1 - Risk Inventory They model infrastructure dependency (what happens if your model provider reprices or restricts access), compliance friction (can this actually survive procurement at a Fortune 500), and talent replaceability (is the technical insight locked in two people’s heads). These aren’t dealbreakers. They’re stress tests. Founders who’ve thought through them build confidence. Founders who haven’t reveal that they’ve been operating in demo mode, not deployment mode. When Microsoft integrated frontier AI into Azure at scale, it accelerated enterprise normalization - but it also concentrated platform power. Startups building on external model layers now operate within dynamic cost and control frameworks. Institutional capital does not reject this risk. It demands awareness of it. The founders who articulate this clearly inspire confidence. Track 2 - Traction Verification This is where most AI founders are underprepared. The question is no longer: do users like it? It’s: does removing it hurt? Institutional traction signals look like:

The Institutional Readiness DiagnosticBefore your next LP or Series A conversation, pressure-test these five questions. Not for an investor for yourself.

If you can answer all five fluently, you’re ready for institutional diligence. If two or three stump you, you know where to spend the next 90 days. The Founder Who Gets Funded NowThe founders raising institutional rounds in 2026 aren’t necessarily the ones with the best technology. They’re the ones who can walk into a room and speak fluently about their cost curve, their model dependency, their expansion logic, and their procurement path without being asked. That fluency signals something specific: that they’ve already done the stress test themselves. AI fundraising didn’t get harder. It got more honest. The magic was always temporary. The mechanism was always what mattered.

See you in the next issue, – Shubham Bopche Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Tuesday, 3 March 2026

The New Rule of EarlyStage AI Fundraising

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment