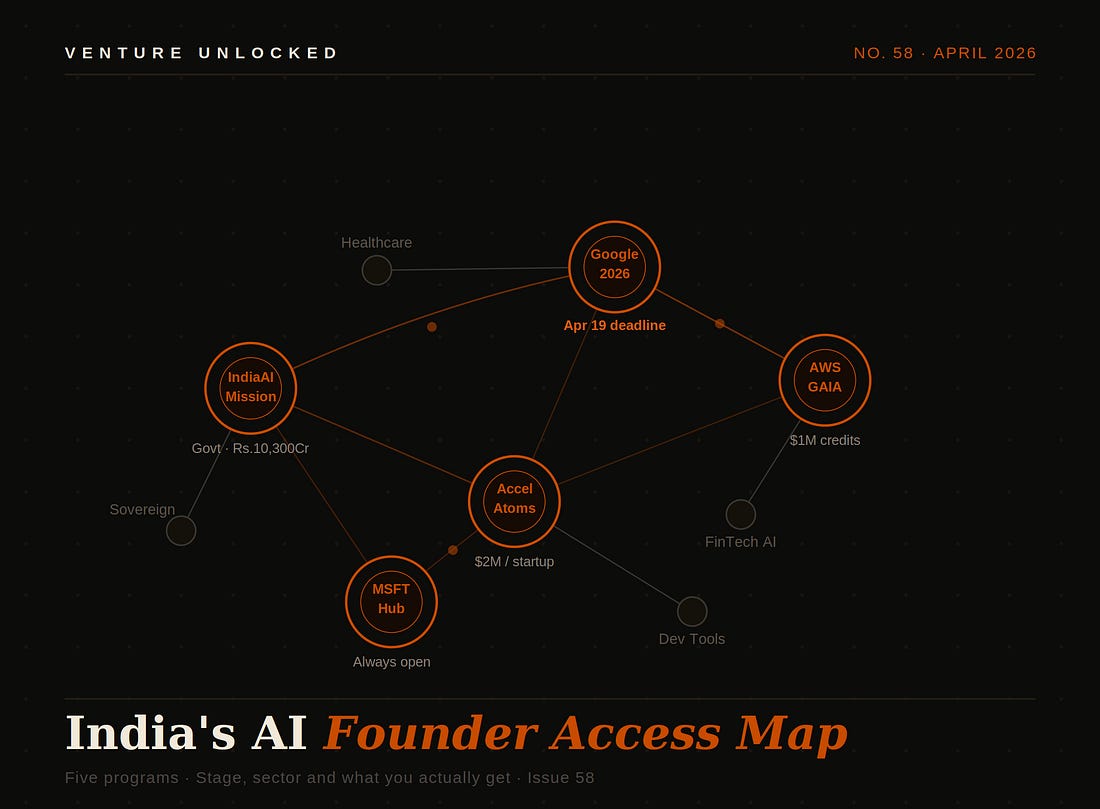

India's AI Founder Access MapIssue 58 : Every major program open to Indian AI founders right now mapped by stage, sector, and what you actually get. No PR framing. Just the map.

On March 31, Google opened applications for its 2026 India accelerator. Deadline: April 19. That is less than three weeks from now. If you missed it, you are not alone. Most founders either do not know these programs exist, or they know they exist and do not know if they qualify, what they offer, or how serious they actually are. The result is that some of the most well-funded and well-staffed AI programs in the country go underused by exactly the founders they were built for. So this issue is a straightforward fix for that. We have mapped every meaningful AI founder program currently active in India government and private with the stage it targets, the sectors that tend to get selected, what you actually receive, and a plain take on which ones are worth your time. Then we will layer in the bigger picture: where India’s AI investment is concentrating, which sectors are attracting the most capital, and what the Q1 2025 numbers actually tell us about where the ecosystem is heading.

SECTION 01 - INVESTMENT LANDSCAPEWhere the Money is Actually Going Before the program map, context matters. The Bain India VC Report 2026 released this week shows India’s VC ecosystem posted $16 billion in funding in 2025, the second straight year of growth. Unlike 2024, where raw deal volume drove the headline, 2025 saw more balanced growth: deal volume up and average deal size up. The bigger signal is where capital concentrated. Software and SaaS saw roughly 1.5x growth year-on-year, with two distinct tiers: mature incumbents from the 2021–22 cycle returning to market on the back of geographic expansion, and younger AI-native B2B companies gaining traction in vertical applications. Fintech posted one of the strongest sector rebounds, with deal value more than doubling and within fintech, wealthtech emerged as a breakout theme, driven by India’s DPI rails and rising household savings. BFSI and healthcare led the charge on AI deployment specifically, with Bain noting that use cases in these sectors have visibly moved from pilots to production-scale automation. Q1 2025 alone saw $3.1 billion across 232 deals, with AI leading investor attention. By July 2025, Venture Intelligence data showed $524 million had gone specifically to Indian GenAI ventures and that number kept climbing. The Indian AI market, valued at roughly $1.25 billion in 2025, is projected to grow at 27.6% CAGR to reach $12.43 billion by 2033. Government officials are forecasting AI’s contribution to India’s economy at $1.7 trillion by 2035. These are not fantasy numbers. They are consistent with what is being built on the ground: Krutrim became India’s first AI unicorn in 2024 on just $74 million raised. Sarvam AI was selected from 67 applicants to build India’s first sovereign LLM. Fractal Analytics, Neysa, Kore.ai, and Observe.AI are all at or near unicorn territory. The infrastructure investment Microsoft at $17.5 billion, Amazon at $35 billion committed through 2030 is not charity. It is a bet on India becoming a production geography for AI workloads. QUARTERLY SNAPSHOT - Q1 2025$3.1B raised across 232 deals. AI sector led investor attention. Bengaluru retained its position as India’s primary AI hub. Hyderabad emerged as a strong second, driven by Telangana AI Mission (T-AIM). Enterprise BFSI and healthcare AI led deployment activity. $250M+ deals doubled year-on-year. Stanford’s 2025 Global AI Vibrancy Tool ranked India third globally, behind only the US and China.

SECTION 02 - SECTOR DOMINANCEWhich Sectors Are Winning Attention and Why Not all AI categories are created equal in India right now. Four sectors are clearly dominating both capital allocation and program selection and understanding why matters if you are building or applying to any of the programs in the next section. ENTERPRISE BFSI AND FINTECH AIThis is the clearest winner. BFSI use cases risk scoring, fraud detection, loan underwriting, customer service automation are not experimental in India anymore. They are in production. AWS GAIA selected Hyperbots from India on the strength of its agentic F&A platform targeting CFOs. Kore.ai raised $150 million. The Bain report explicitly calls out BFSI as having moved from pilots to full-scale deployment. If you are building AI for financial services, you are building in the hottest lane. SOVEREIGN AND INDIC LANGUAGE AIThis is the most uniquely Indian opportunity on the map. India has 22 constitutionally recognised languages, 1,500+ dialects recorded by census, and over a billion people who are not fluent English speakers. The IndiaAI Mission is explicitly investing in this gap. Sarvam AI’s selection as the government’s sovereign LLM partner building models that run four to six times faster than competitors in Hindi and 10 regional languages is the clearest signal. Google’s 2026 accelerator has a dedicated Sovereign AI track. Vaani AI, another Google accelerator alumnus, processed over one million minutes monthly and cut manual calls by 75% using Gemini and its own foundational model. HEALTHCARE AIHealthcare is where India’s scale advantage is most visible. AiSteth, a Google accelerator alumnus, built an offline smart stethoscope that screened over 75,000 patients across 20 states without an internet connection. Qure.ai, near unicorn status, is doing diagnostic imaging at population scale. The IndiaAI Mission has approved 30 India-specific AI applications, with healthcare among the top categories. The combination of government backing, large addressable population, and low existing infrastructure makes healthcare AI one of the most funded and program-favoured sectors right now. AGENTIC AND DEVELOPER INFRASTRUCTUREGlobally, multi-agent AI system inquiries surged 1,445% from Q1 2024 to Q2 2025. India is catching this wave fast. Accel Atoms explicitly frames its 2026 AI cohort around the ‘Future of Coding’ thesis investing in founders who shift software from engineering to orchestration. Google’s 2026 accelerator has a dedicated Agentic AI track. Superjoin, an Accel and Google-backed company, improved accuracy and latency by 50% using Gemini 3.0. Developer tooling and infrastructure for agent deployment is early but attracting serious VC attention. SECTION 03 - THE PROGRAMSEvery Open Door for Indian AI FoundersFive programs dominate the current landscape. Two are government-led. Three are private. Together, they cover almost every stage from idea to Series A and between them offer everything from subsidised compute to co-investment to a global launchpad. Here is each one, in plain language.

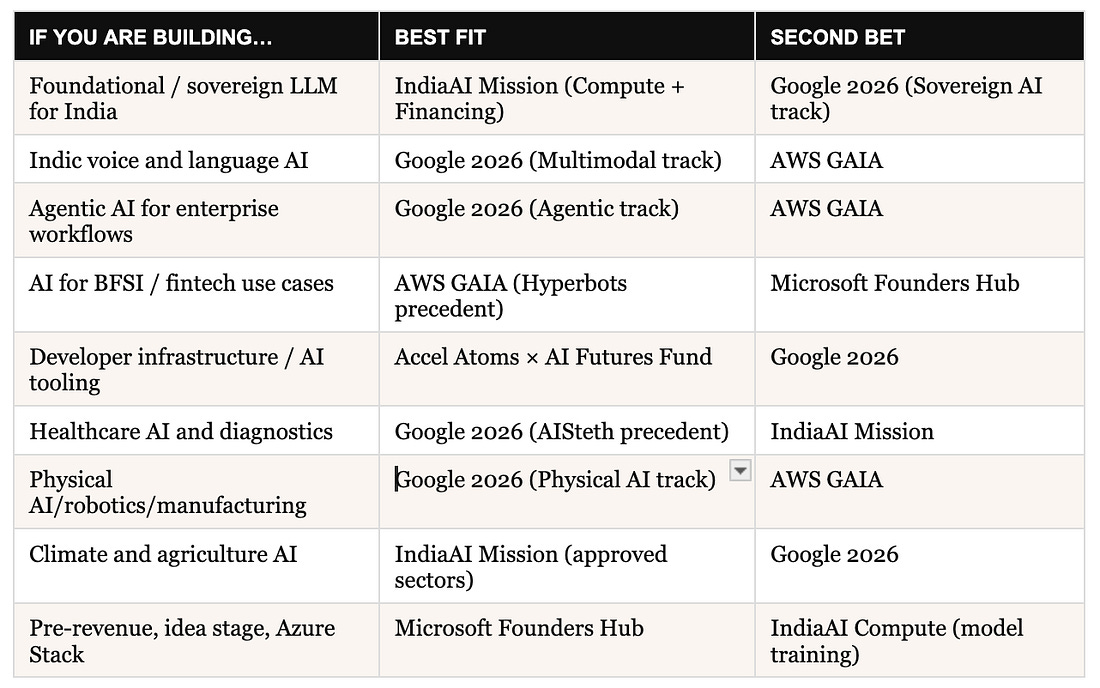

SECTION 04 - THE MAPWho Should Apply for WhatNot every programme fits every founder. Below is a decision map based on what each programme has actually selected, funded, and rewarded not what their websites say they care about.

SECTION 05 - THE HONEST TAKEWhat Founders Get Wrong About These ProgrammesRead these programmes together and a pattern becomes clear: every major tech company is running an accelerator for the same structural reason to lock in the next generation of AI-native companies onto their infrastructure stack before they grow large enough to choose freely. Google wants Gemini integrations. AWS wants workloads on AWS. Microsoft wants Azure commitments. That is not a criticism. It is an honest framing. The programmes are genuinely valuable the mentorship networks, compute access, and model integrations are real, not ceremonial. But the long-term cost is potential platform dependency. Founders who do not think about this early often find themselves rebuilding their technical stack at Series B, at precisely the moment when execution speed matters most. The founders who navigate this well do three things. First, they enter with a clear thesis about which platform relationships actually match their product architecture not just which programme has the best credits. Second, they use programme resources to reach a specific milestone (first enterprise contract, first production deployment, first revenue cohort) rather than treating the programme as an end in itself. Third, they preserve optionality: take the credits, take the mentorship, but do not let programme relationships substitute for independent commercial validation. The IndiaAI Mission is structurally different government-backed, sector-agnostic by design, and not trying to sell you infrastructure. But it has its own version of the same trade-off: slower access, stricter eligibility, and a bureaucratic process that favours well-connected startups with clean legal structures over nimble early-stage teams building fast. The compute is genuinely world-class. The path to access it is not frictionless.

India now has more structured support for early AI founders than at any point in its history. The compute is real. The co-investment is real. The mentorship networks are real. Globally, AI funding hit $238 billion in 2025 up 109% year-on-year and India is capturing an increasingly meaningful share of that attention. What is not guaranteed is that your application lands. Every programme on this list is selective and the ones that are not selective compensate with lower intensity. The April 19 Google deadline is not a nudge. It is a wall. If you are building something serious in AI and have not applied to at least one programme yet, start this week. The founders who will define India’s AI decade are not waiting for a better moment. They applied last week. If you found this useful, forward it to one founder who needs it more than you do. Shubham Bopche - Editor Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Sunday, 5 April 2026

India's AI Founder Access Map

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment