PE didn’t pause. You just weren’t watchingIssue 60 : While founders watched VC dry up, a quieter $48 billion was moving differently.

In 2025, India’s private equity market did something that most founder conversations missed entirely. Deal volumes declined 8%. Total transaction value rose 23%. Fewer deals. More money. That’s not a contraction that’s a concentration. While early-stage VC was the story everyone was telling who raised, who didn’t, which fund dried up a quieter, larger capital reallocation was underway. PE wasn’t pausing. It was getting more deliberate.

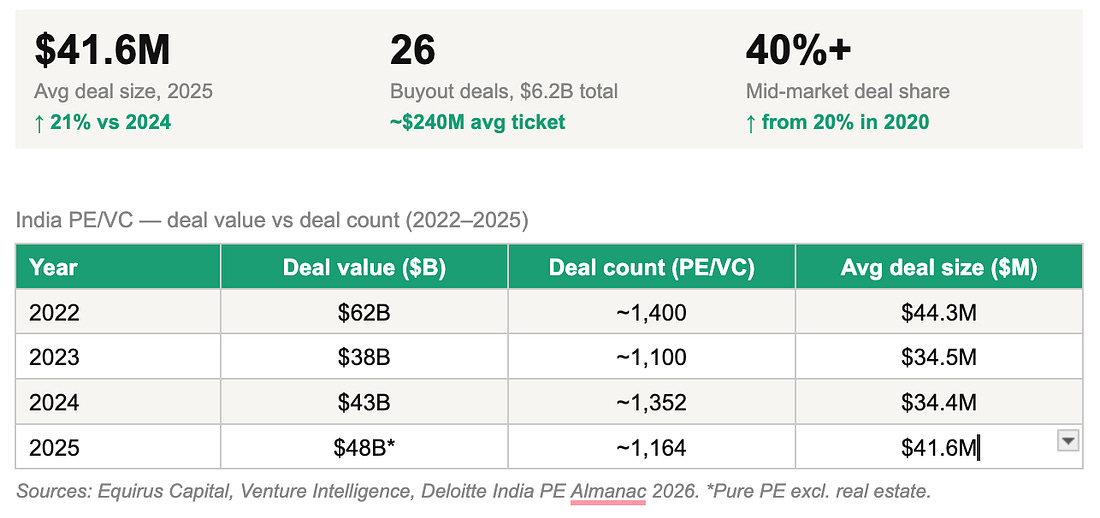

What 2025 actually looked likeThe headline number depends on who’s counting. Equirus Capital tracked 1,761 PE/VC deals between January and November 2025. A 10-year high in volume terms, surpassing even the 2021 peak. But aggregate deal counts include everything from seed-stage VC to large buyouts. When you isolate pure-play PE, the story is different. Deal concentration was the defining theme. Average deal size grew from $34.4 million in 2024 to $41.6 million in 2025. Buyouts alone just 26 transactions accounted for $6.2 billion, averaging roughly $240 million per deal. Mid-market deals in the $10–50 million range expanded from under 20% of deal count in 2020 to over 40% in 2025.

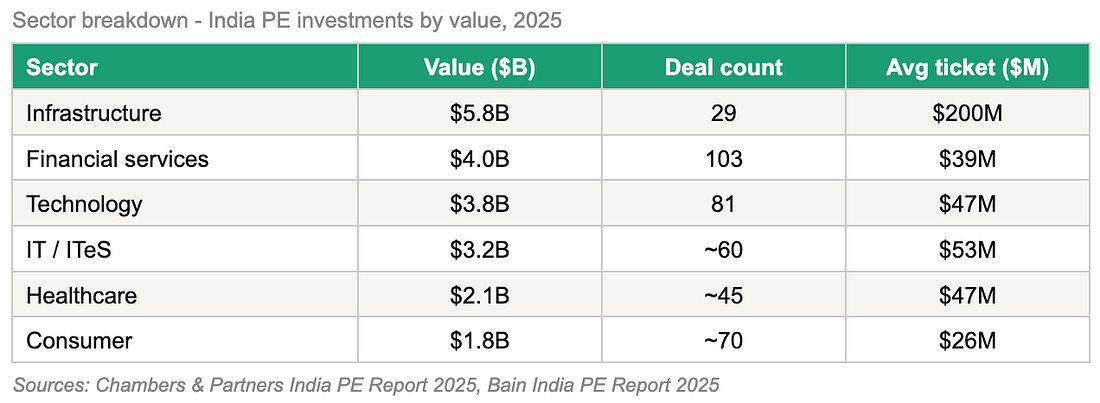

The exit environment told the same story. The number of exits fell 53% in 2025. Exit value fell only 15%. Trade sales strategic acquirers buying PE-backed companies surged 154% in value. Investors weren’t rushing out. They were waiting for the right door, and holding longer to find it. Where the money actually wentSector allocation in 2025 showed a clear hierarchy. Infrastructure led on ticket size is $5.8 billion across just 29 deals reflecting patient, long-duration capital going into roads, power, and data infrastructure. Financial services came second at $4 billion across 103 deals, driven by affordable housing finance, loan against property, and MSME lending. Technology sat at $3.8 billion across 81 deals. The surprises were elsewhere. IT and ITeS investments surged approximately 300%, driven by major deals like Perficient and Altimetrik alongside a wave of revenue cycle management investments. Healthcare deal volumes rose roughly 80%, led by medtech transactions and pharma CDMO plays. These are not glamorous consumer-facing bets these are operational businesses with defensible revenue models and global demand tailwinds.

Global funds recalibrated alongside domestic ones. KKR committed up to $310 million into PMI Electro Mobility an Indian electric commercial vehicles company emblematic of the new thesis: infrastructure-adjacent, energy transition, long-duration. PwC’s 2026 M&A outlook found that more than one-third of capital from newly raised Asian PE funds is now being directed toward India.

Domestic capital formation of this scale tells you something: India’s LP base is growing up alongside its GP base. The money isn’t just coming from outside anymore.

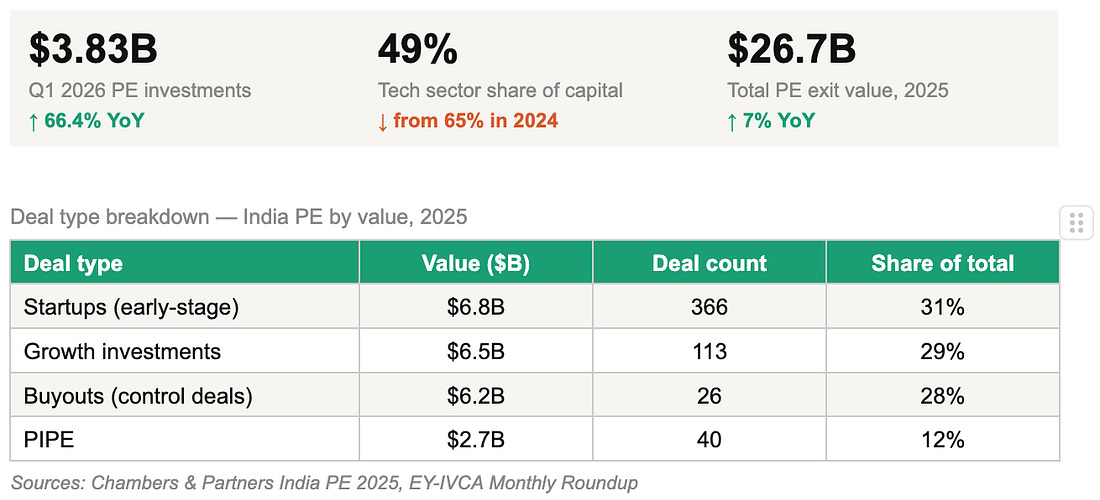

What 2026 is already signalingQ1 2026 came in at $3.83 billion up 66.4% year-on-year and the strongest opening quarter in two years. Technology-led sectors still dominated at 49% of capital deployed, but that share is declining from 65% the previous year. The distribution is broadening. Energy sector investments surged, aligned with India’s energy transition agenda. Improving public market exits, if they sustain, create a positive feedback loop: clearer exit visibility encourages new deployment.

But the near-term picture is not clean. EY’s Vivek Soni framed 2026 as a “wait-and-watch” environment, investors assessing earnings visibility and whether the bid-ask spread between buyers and sellers will narrow. Geopolitical variables, particularly the Iran-Israel-US conflict and its downstream impact on crude oil prices, remain the single most unpredictable input in the near term. Valuation resets are the quieter tension. PE funds contended with rich valuations through 2023 and 2024, driven by buoyant public markets. As those multiples settle closer to historic norms in 2026, PE activity should increase but selectively. The discipline built over the last two years isn’t going away. India’s PE ecosystem has, in Deloitte’s words, shifted toward a “more mature and disciplined investment landscape.” That phrase carries real weight for anyone thinking about where the entry bar now sits. THE THING NOBODY IS SAYING OUT LOUD

Shubham Bopche - Editor Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Monday, 20 April 2026

PE didn’t pause. You just weren’t watching

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment