From the PE room to Dalal StreetIssue 61 : What changes between PE-ready and IPO-ready and why most founders find out too late

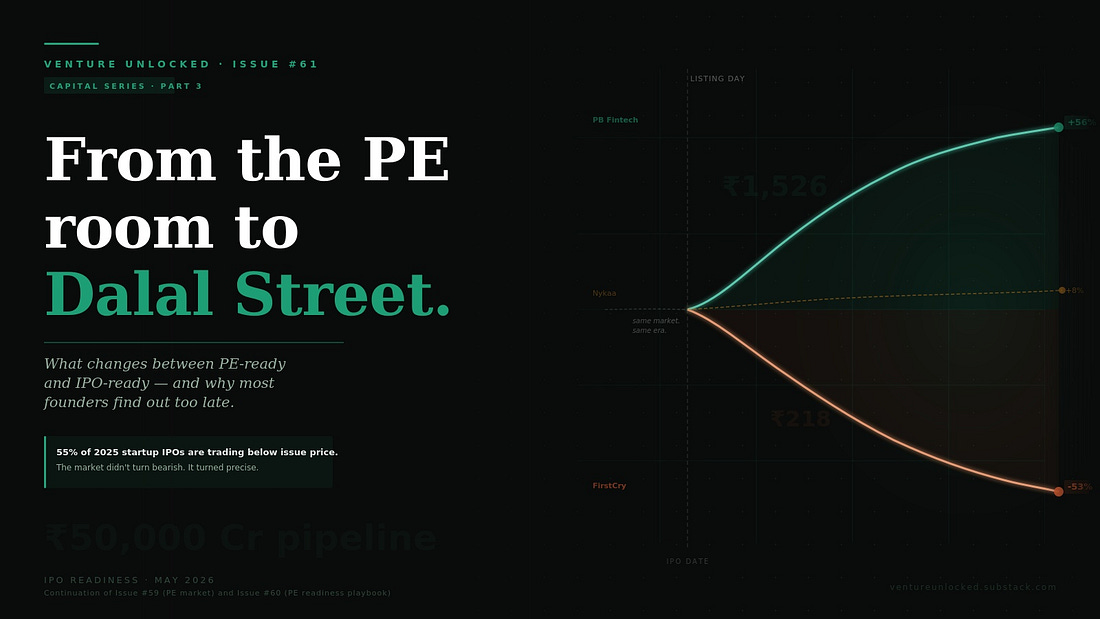

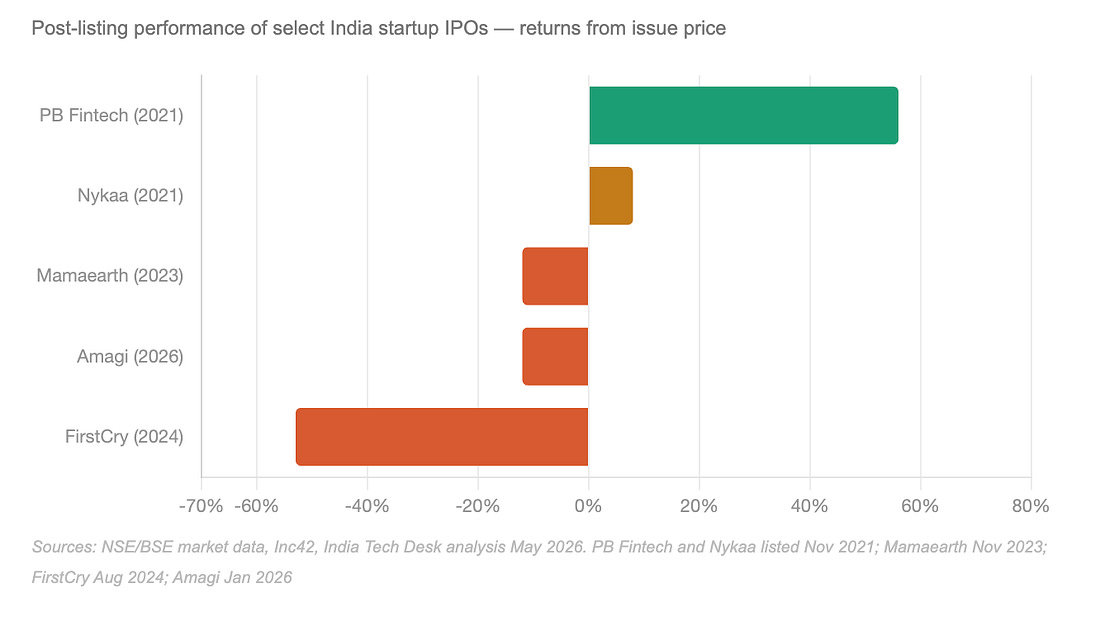

In November 2021, two Indian startups listed on the same exchange, in the same market, within weeks of each other. PB Fintech the parent of PolicyBazaar - priced at ₹980. Nykaa priced at ₹1,125. Both were celebrated as landmarks. Both were massively oversubscribed. Four years later, PB Fintech trades at ₹1,526 thats up by 56%. Nykaa has delivered an annualised return of roughly 8%. FirstCry, from the same vintage, has lost more than half its IPO value. Mamaearth is down 12% from its listing price. Same market. Same investors. Same era. Completely different outcomes. The difference was never the market window. It was what each company looked like underneath revenue quality, unit economics durability, governance infrastructure, and whether the business had been built for public scrutiny or just for the next private round.

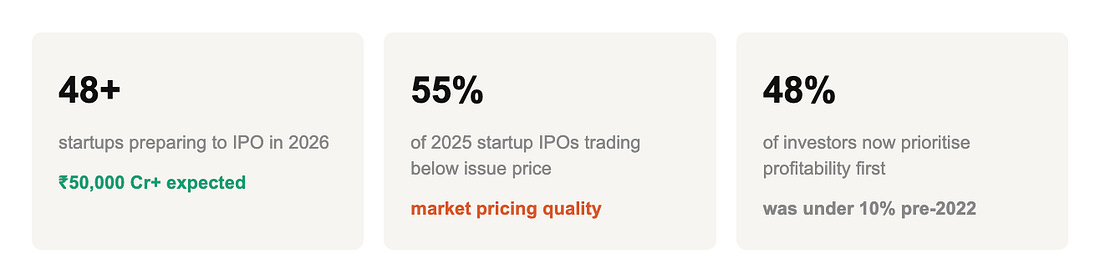

Section 01 What the 2026 pipeline actually looks likeIndia’s IPO market in 2025 was its busiest ever for new-age tech. Eighteen startups raised ₹41,248 crore collectively. The 2026 pipeline is even larger Zepto, PhonePe, OYO, InMobi, Zetwerk, Flipkart, and potentially Razorpay are all in various stages of preparation. Unicorns and decacorns lining up for domestic listings within the same 18-month window. But underneath the headline numbers, the composition of the 2025 cohort tells a cautious story. Of ₹41,248 crore raised, ₹21,474 crore - 52% came through Offer for Sale components. Existing investors selling out, not fresh capital entering businesses. And public market investors, who have now lived through the post-listing performance of that cohort, are adjusting accordingly.

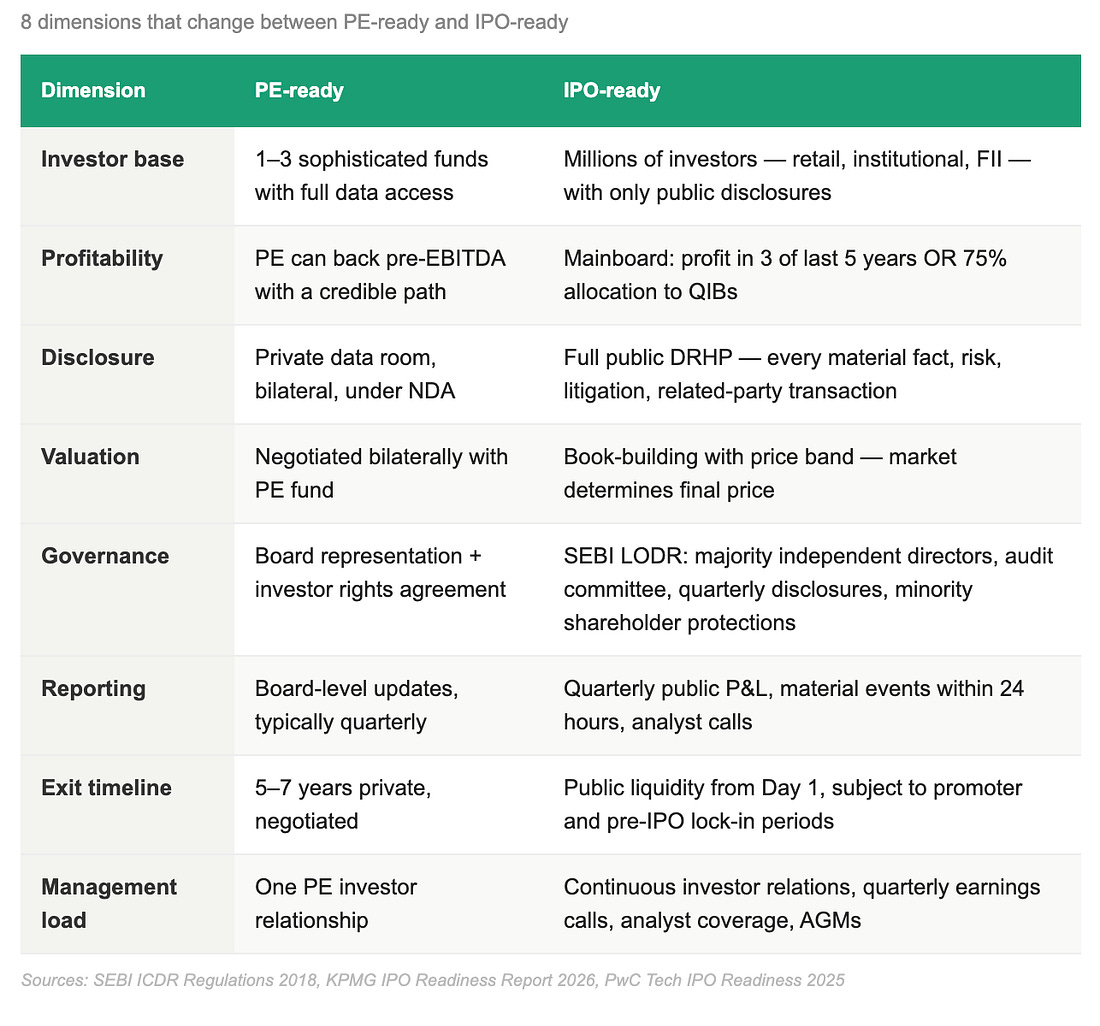

The 2026 filter is more demanding. Retail subscription rates moderated from 34.15x in 2024 to 26.42x in 2025. FIIs are more cautious. And a crowded calendar — potential mega-IPOs from Jio and SBI Mutual Fund could absorb significant liquidity — means mid-size startups will compete harder for attention than in a thinner market. “IPO-bound startups in 2026 will be increasingly defined by their ability to demonstrate predictable cash flows, sustainable unit economics, and operational discipline rather than headline growth alone.” Section 02 PE readiness vs IPO readiness - what actually changesMost founders treat PE and IPO as points on the same continuum. They are not. PE is a bilateral negotiation with one or a few sophisticated counterparties who have full data room access. IPO is a public process regulated by SEBI, scrutinised by retail investors, institutions, and FIIs simultaneously, and then governed on a quarterly basis permanently.

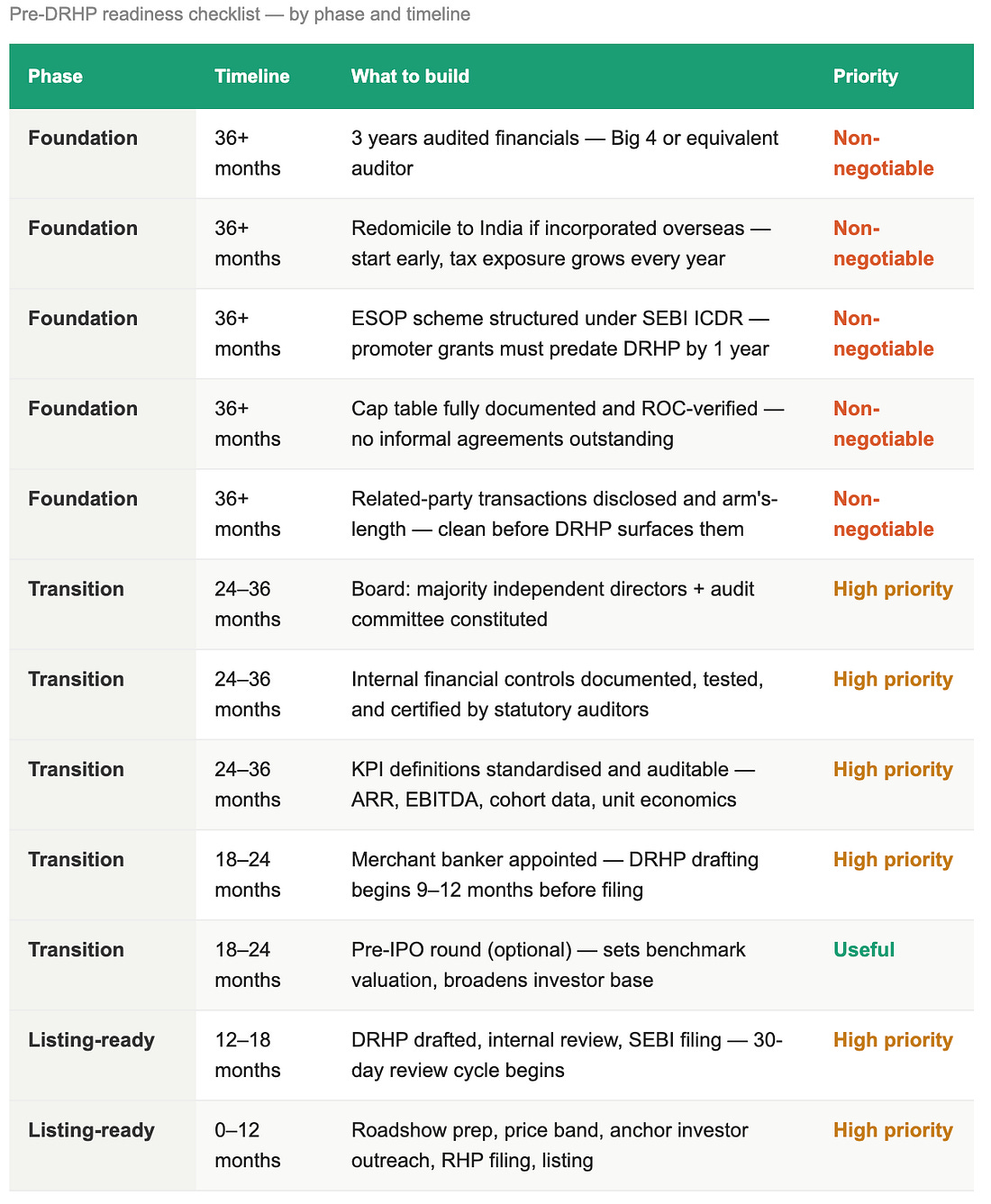

65% of companies disclosed material weaknesses at IPO up 15% from prior years primarily due to inadequate technology systems and undocumented internal financial controls. These are not disclosure failures. They are operational failures that surface because public companies must certify their controls, not just present their numbers.

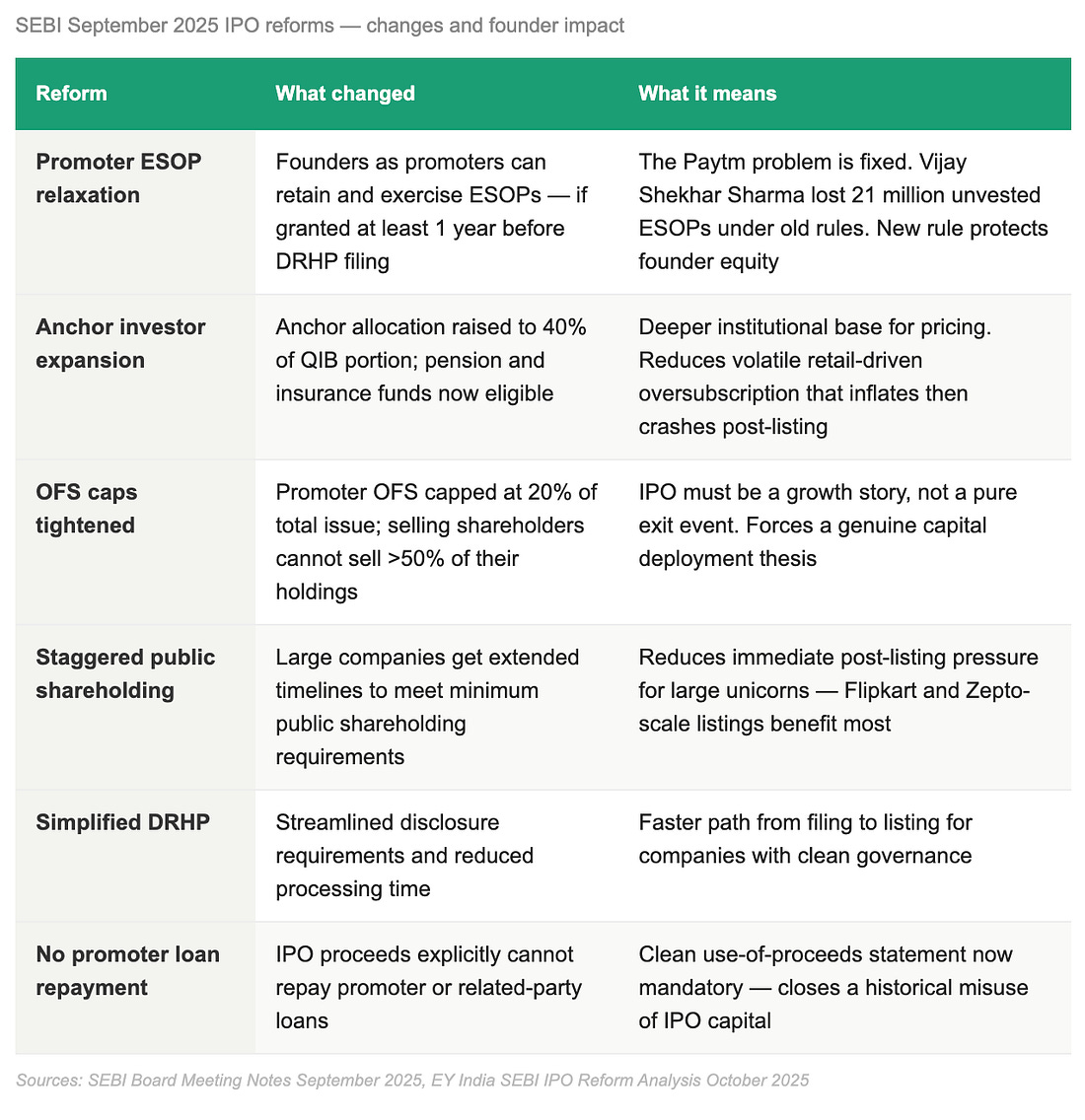

Section 03 SEBI’s September 2025 reforms - what actually changedSEBI’s September 2025 overhaul was the most significant reform to India’s listing rules in a decade. It addressed three structural problems slowing startup listings and introduced one change that specifically benefits founders preparing for public markets.

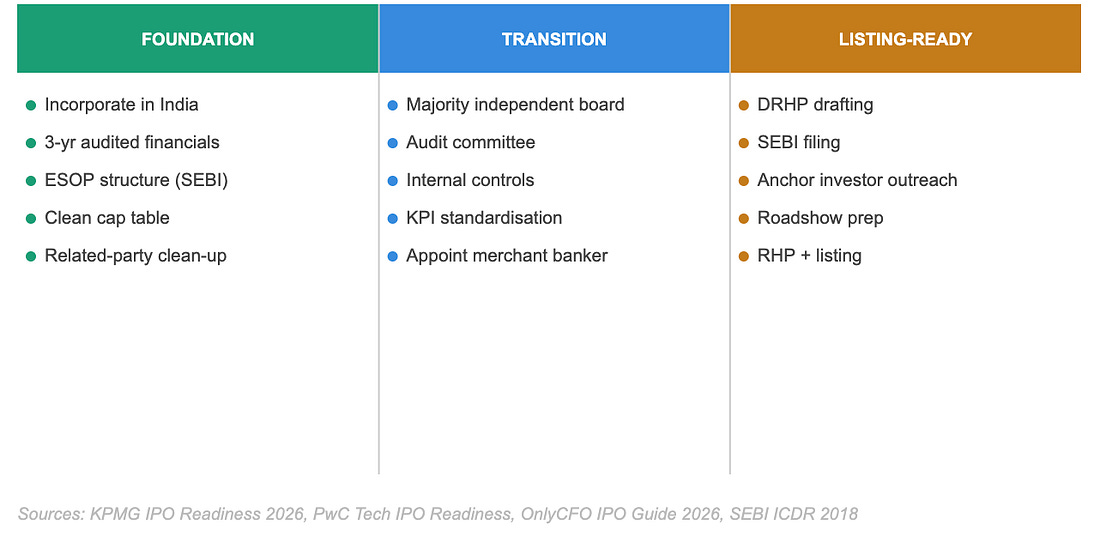

One reform that did not make headlines but matters: SEBI’s October 2025 ban on mutual fund participation in pre-IPO placements. Previously, hybrid and thematic funds had deployed an estimated ₹3,000–4,000 crore into pre-IPO holdings using internal valuation models — essentially pricing companies without public market discipline. Its removal forces pre-IPO valuations to anchor to what institutional investors and family offices will actually pay. More conservative. More durable. Section 04 What to build 24–36 months before you file a DRHPCompanies that begin IPO preparation 18–24 months before listing have the highest likelihood of completing the process without material weaknesses or timeline slippage. Those that start 6 months out face expensive remediation under time pressure. KPMG’s 2026 governance framework frames IPO readiness as a “continuum of progressive institutionalisation” across three phases. Most founders think they are in the transition phase when they are still in foundation.

The item that most consistently derails Indian startup IPOs is the redomiciliation - moving from Singapore or Delaware back to India. PhonePe lost $900 million in accumulated losses and paid ₹8,000 crore in tax liabilities. Groww incurred a $160 million US tax bill. Razorpay slipped into the red due to ₹1,209 crore in ESOP expense and tax payments tied to its reverse flip. Three of the most prominent Indian startup IPO stories of the last three years all tracing back to an incorporation decision made at Series A or earlier. 📌 If you’re at Series A - read this section Everything in this issue describes decisions made 36 months before a DRHP is filed. If you’re at Series A, that timeline starts now not when you’re Series C and suddenly PE-adjacent. Three things to do in the next 90 days based on what this issue covers:

Issue #62 goes deeper - the six Series A decisions that determine whether PE and IPO are options at all, with named India examples and a practical fix for each The Market Has Already Decided The 2026 IPO pipeline is not evidence that public markets are easy. It is evidence that a large number of Indian founders believe they are ready and that the market will sort out who actually is. The sorting mechanism is already visible in the data. PB Fintech up 56%. FirstCry down 53%. Same market, same year, same investor base. The difference was operational governance infrastructure, profitability clarity, and revenue quality that could survive quarterly public scrutiny. PE readiness gets you to the growth stage. IPO readiness is a different architecture built over 24–36 months, not assembled in the six months before a DRHP is filed. The founders navigating this most successfully in 2026 are not the ones who raised the most. They are the ones who built the right shape of company while everyone else was focused on the next private round. The window is open. The question is whether you built for it. Shubham Bopche - Editor Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Sunday, 10 May 2026

From the PE room to Dalal Street

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment