The Anatomy of a Listable CompanyIssue 64 : Same IPO window, Opposite endings. What separates the companies the market rewards from the ones it punishes, and how early that's actually decided.

Two companies ring the bell in the same window, the same year, under the same euphoric listing-day headlines. One keeps climbing. The other starts sliding within weeks and never recovers. Nothing in the press release told you which would be which, but the market knew inside a quarter. Last issue ended on a question: if the only exit that returns real cash is the public market, then are you listable? Here’s what I’ve come to think after watching this cohort list. The market has stopped treating that as a yes-or-no decided on listing day, and started treating it as something it can measure, well in advance. This issue is about what it measures, and when the measuring actually starts.

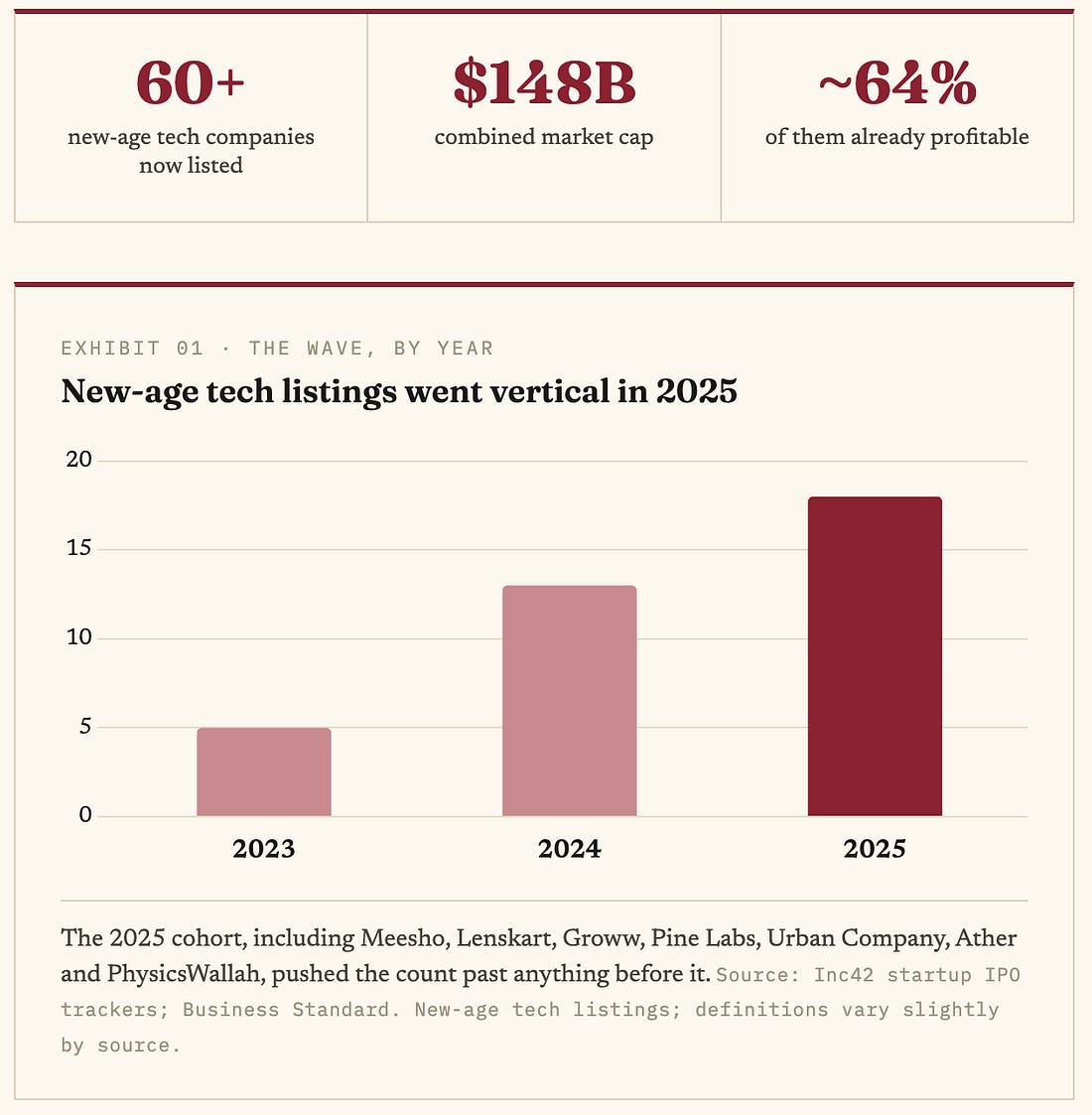

The Market Started DiscriminatingFirst, the scale, so we're clear this isn't a niche story anymore. More than 60 new-age tech companies are now listed in India, worth a combined $148 billion-plus, and roughly two in three are already profitable. The wave built fast, and 2025 was its peak.

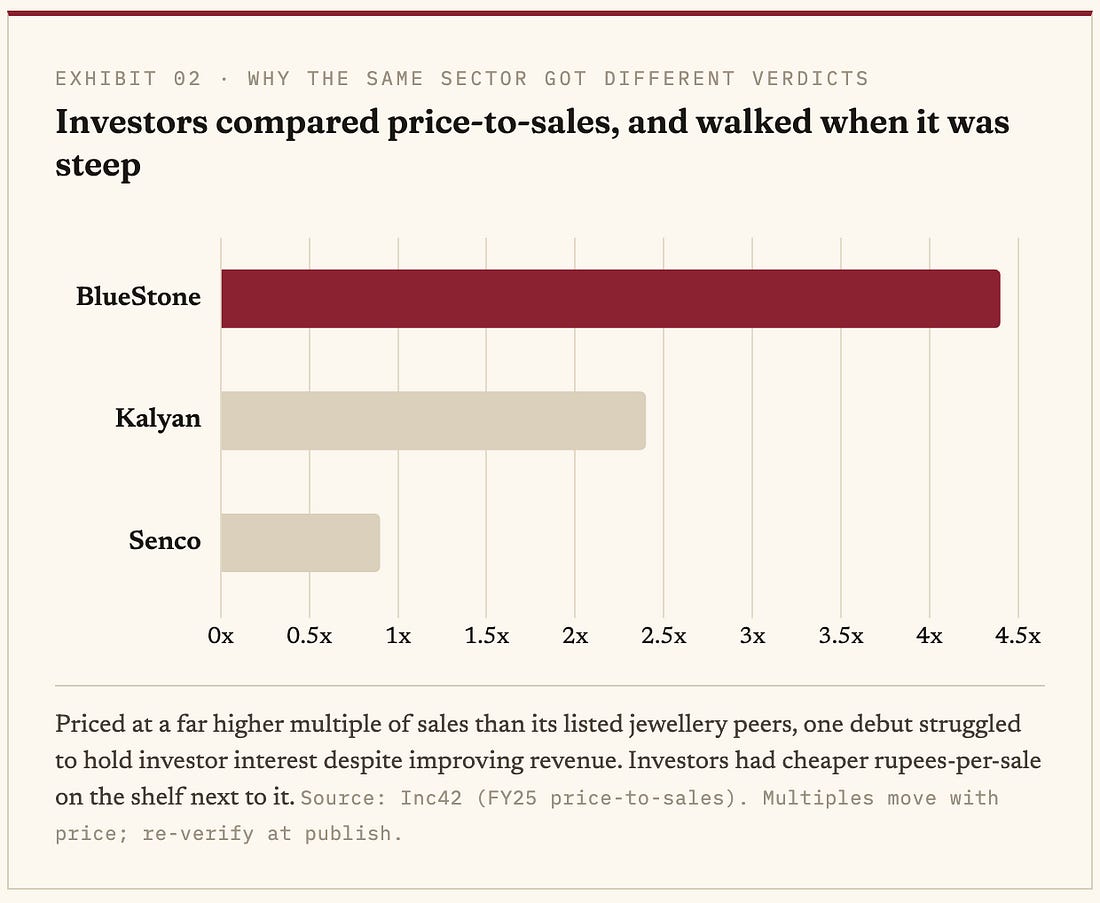

But the number that matters isn’t how many listed. It’s how differently they did once they were public. The wave stopped lifting every boat equally, and that’s the genuinely new thing. The moment outcomes spread this wide, “listable” stops being a vibe and becomes a checklist the market is quietly running on you. The Anatomy of a Listable CompanySo what is it actually checking? Reverse-engineer it from who rose and who sank, and four traits keep showing up. One. Profitability, or a believable path to it. The 2021 cohort listed on growth stories. The 2025 winners listed on profit, or a clear line to it. Lenskart, for one, swung to a roughly ₹297 crore net profit after a small loss the year before, exactly the kind of turn the market now wants to see before it commits. Two. A valuation the market can defend. This is where it gets brutal, and it’s one of the clearest signals in the whole cohort.

Groww and Meesho, priced sensibly, climbed after listing. The ones that demanded a premium the fundamentals couldn’t carry faded once the listing-day adrenaline wore off. The market isn’t anti-ambition. It’s just doing comparison shopping you no longer control. Three. Founders who aren’t sprinting for the door. Heavy promoter selling at the IPO reads, fairly or not, as “the people who know this best want out.” Four. A story that survives the afterparty. Anything riding pure listing-day sentiment slid the moment the sentiment did.

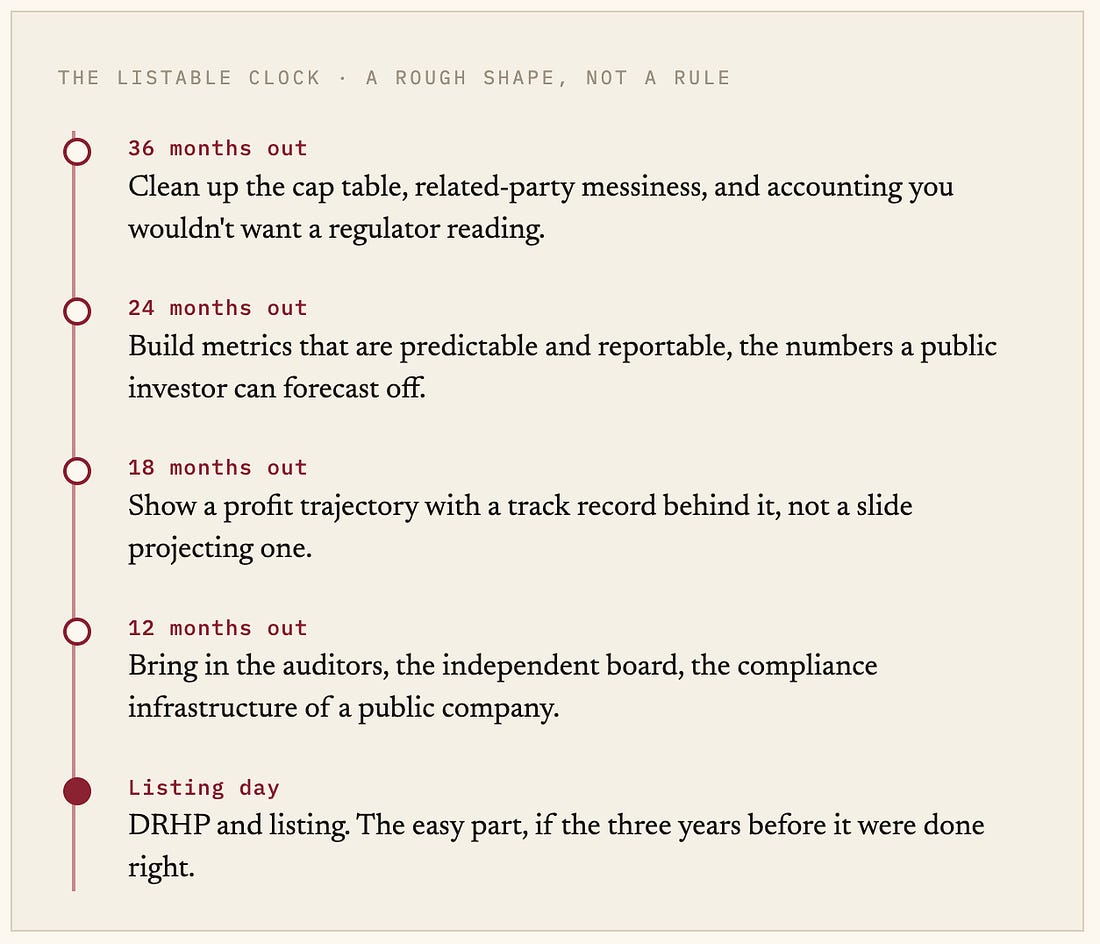

The Clock Starts Years Before the BellHere’s the part founders underrate most. None of those four traits can be manufactured in the two quarters before a DRHP. Audit-grade financials, metrics that are predictable enough to forecast, clean governance, a profit trajectory with a track record behind it. These are states you grow into, not boxes you tick in the last lap.

There’s one node on that clock I’d underline, because it’s the one I watch companies discover too late. Of the four readiness states, governance and audit-grade reporting are the only ones you genuinely cannot sprint. Profitability can sometimes be pulled forward by a hard quarter of cost cuts. A clean controls layer cannot, because it isn’t a number you produce. It’s the trail you left behind you. How consistently the records were kept. Whether your data, your consents, and your related-party flows hold up when an independent reviewer reads them backwards. Whether the controls existed at the moment each transaction happened, or were reconstructed afterward to satisfy the bankers. By the time a DRHP is being drafted, diligence reads that history, not your intentions. A company that started keeping public-company records three years early walks through it in weeks. A company that decides to clean up twelve months out spends those months in remediation it cannot fully finish, and the gaps surface in the offer document for every investor to price. The unglamorous infrastructure is the part that quietly decides whether the other three traits even get a fair hearing. The read I keep landing on: the companies that listed well started looking like public companies long before they had to. Which means the decisions that make you listable in 2028 are the ones you’re making, or quietly skipping, right now. What I’d be watchingNot advice, you know your own numbers. But depending on where you sit, this is the signal I’d track. If you’re a founderRun the four traits against yourself honestly. Which are you missing, and is your runway to IPO long enough to actually fix them, or are you hoping to paper over a gap in the final two quarters? The gap usually wins. If you’re a VCWatch whether you’re nudging a company toward a window it isn’t built for yet. A rushed listing is a bad exit wearing a good exit’s clothes, and the market undresses it within a quarter. If you’re an operator weighing an offerAsk whether “we’re going public” is a near-term liquidity event or a three-year rebuild. Those are very different ESOPs. Price the offer to the honest answer, not the pitch. Next issue · #65 Which leaves the question I want to sit with next, and it’s the uncomfortable inverse of this one. Suppose you are listable, with clean financials, real profit, and a price you can defend. There’s still a harder question hiding underneath it: should you list at all? Some of the strongest companies in this cohort might have been better off never ringing the bell. That’s #65. See you in the next one, Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Monday, 15 June 2026

The Anatomy of a Listable Company

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment