A growing set of Indian companies have filed to list, withdrawn, and come back years later. What changes between the two filings tells you more than either filing does on its own.

In October 2021, Oravel Stays filed to raise ₹8,430 crore. In July 2026, the company still has not listed. In between it filed three times, withdrew twice, changed its name to PRISM, and revised its target valuation down from around $12 billion at the first attempt to roughly $8 billion at the current one. Nearly five years have passed. The easy way to read that is as a failure story. It is not. The company filing now is a structurally different business from the one that filed in 2021, and the gap between the two filings is where all the useful information sits. OYO is also not alone. There is now a visible cohort of Indian companies that tried, stopped, and came back. This issue looks at that cohort, at what actually changes between attempt one and attempt two, and at the one thing that almost never changes no matter how many years pass.

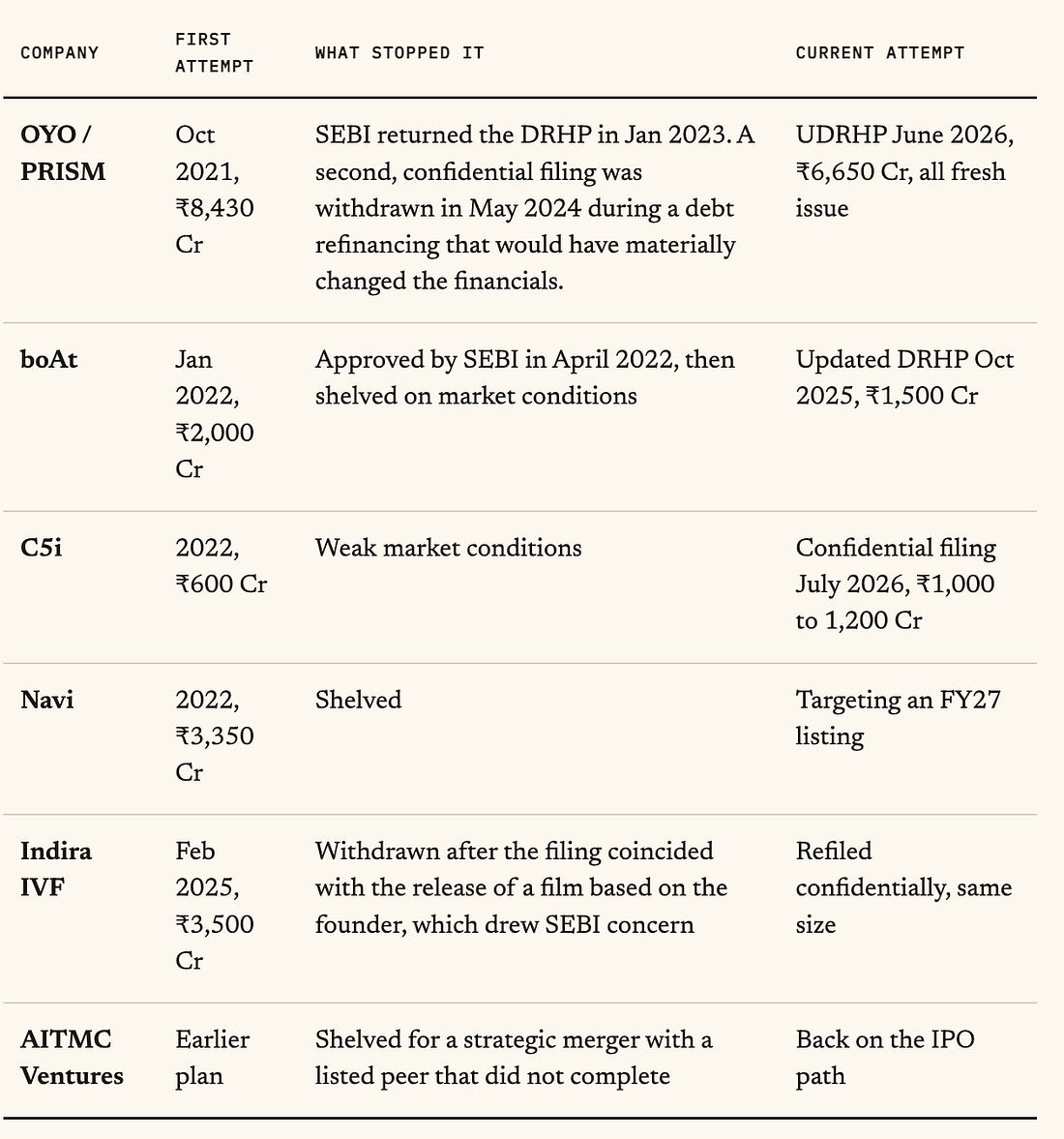

The cohort is bigger than you thinkSix companies, one pattern. The gaps range from under a year to five years.

Section twoWhy this cohort suddenly existsBefore November 2022, withdrawing a DRHP was a public event. The filing was already in the open, the numbers were already being picked apart, and pulling back was read by the market as a verdict on the company rather than on the window. Then SEBI introduced the confidential pre-filing route. Every second attempt in the cohort above has used it: C5i, Indira IVF, InCred and OYO all went in confidentially. The consequence is not a technical one. The cost of a failed attempt has collapsed.

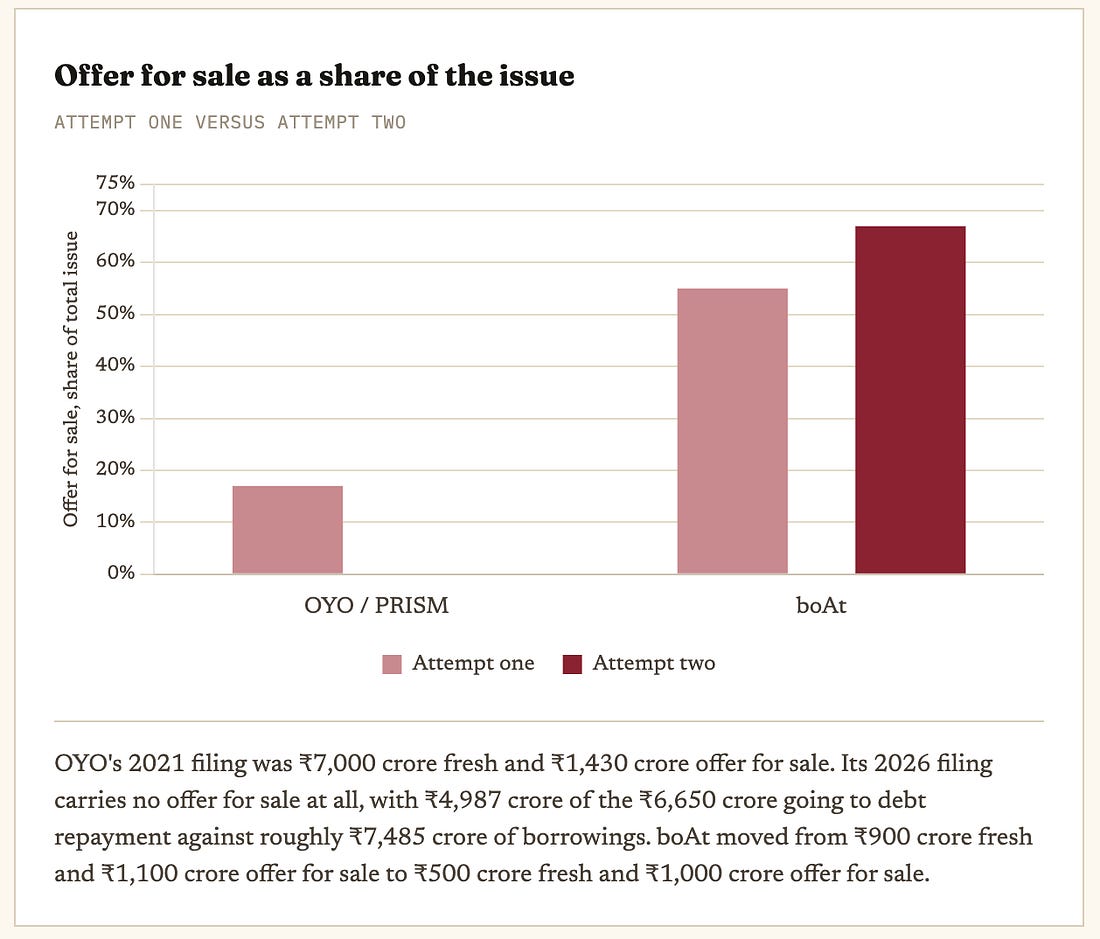

That reframes what a first attempt is. It used to be a commitment. It is now closer to a diligence exercise on yourself, run under regulatory supervision, with a private exit if the answer comes back unflattering. The cohort is growing partly because coming back is no longer embarrassing. Section threeSize is not the tell. Structure is.The intuitive assumption is that companies come back smaller and humbler. The data does not support it. OYO cut its ask from ₹8,430 crore to ₹6,650 crore. boAt cut from ₹2,000 crore to ₹1,500 crore. But C5i came back roughly twice as large, moving from ₹600 crore to a ₹1,000 to 1,200 crore range, and Indira IVF refiled at exactly the same ₹3,500 crore it withdrew at. Issue size moves with the market and with the size of the business. It tells you very little about whether anything was fixed. What does tell you something is who is selling. Compare the two companies in this cohort where both filings are public in full.

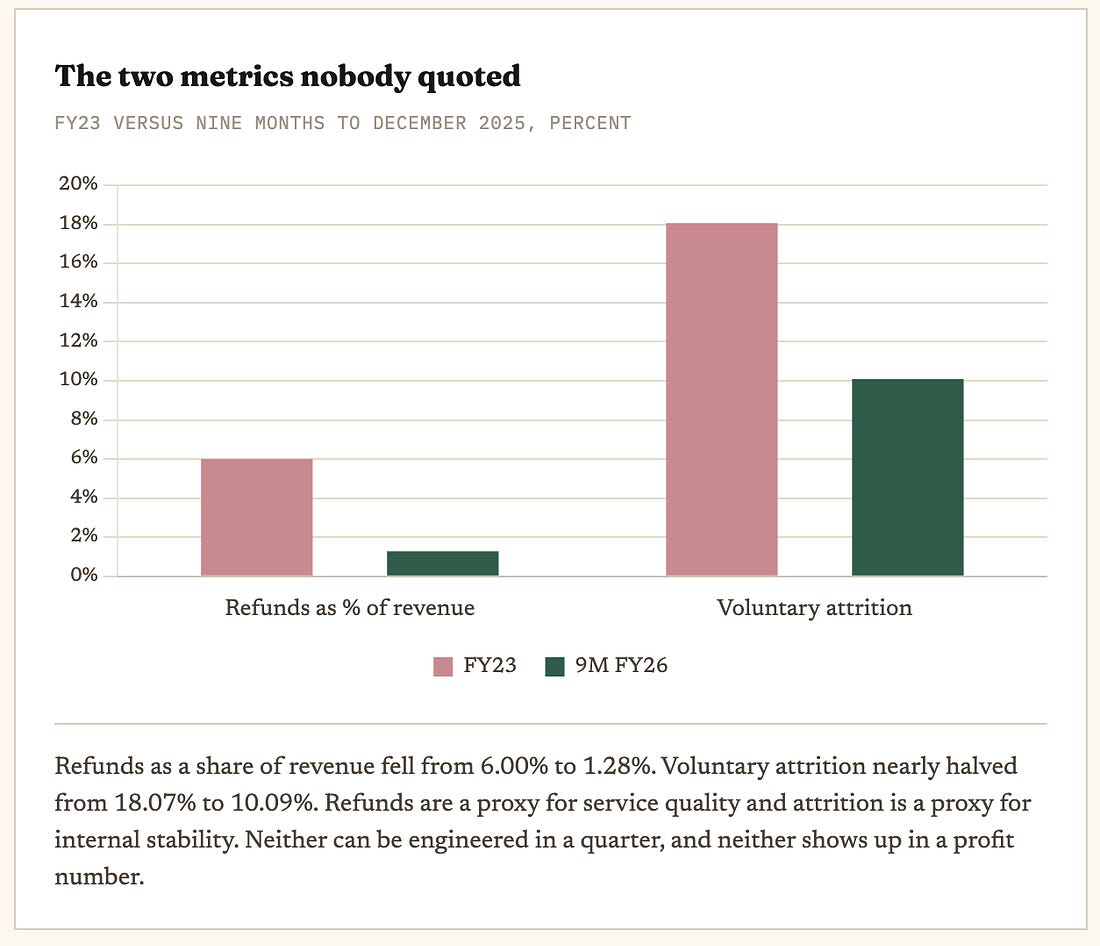

The founder line inside boAt’s two filings is sharper still. In the 2022 DRHP, Aman Gupta and Sameer Mehta were selling ₹150 crore between them. In the 2025 filing they are selling ₹300 crore, with Gupta at ₹225 crore and Mehta at ₹75 crore, on an issue that is 25% smaller. Fireside Ventures and Qualcomm Ventures joined as selling shareholders alongside them. There is a legitimate reading of that. boAt turned around from a loss to a profit of ₹61.08 crore in FY25 on operating revenue of ₹3,070.38 crore, and both founders stepped back from executive roles ahead of the filing, with Gaurav Nayyar taking over as chief executive. Selling into a listing after handing over operational control is a coherent sequence, not a red flag on its own. Meesho went the other way. Ahead of its listing it cut its offer for sale by 40%, with Elevation Capital and Peak XV trimming their quotas, and it is now the benchmark every other listing in this cycle gets measured against. Three companies, three different answers to the same question. That question is the most portable thing in this issue, and we come back to it at the end. Section fourWhat four years of work actually fixedOYO’s current filing is the most complete before-and-after document in the cohort, because the same business has now been described to the regulator three times across five years. The operational improvement in it is real, and it is not the profit line that makes the case. For the nine months to December 2025, PRISM reported a net profit of ₹748 crore, close to three times its full year FY25 figure, on operating revenue of ₹6,941 crore, up around 11%. That is the headline everyone quoted. The two numbers underneath it are more convincing.

So the business improved. That is the part of the story that gets written up. Here is the part that does not. The same updated DRHP carries 99 risk factors and 174 pending proceedings with an aggregate amount of roughly ₹4,435 crore. The list includes the Zostel dispute that dates back to 2015 and still sits as an overhang on the shareholding, a human trafficking litigation in the United States, disputes in Europe, a promoter level tax dispute involving SoftBank’s India holding entity, a competition regulator penalty, and a pledged promoter stake. Every one of those existed at the first attempt. Five years, two withdrawals, a rebrand and a full operational turnaround later, they are still in the document, and now they are being disclosed at length rather than resolved. Our readIn the last issue we argued that audit grade controls cannot be constructed retrospectively, and that the gap shows up in the offer document for every investor to price. This cohort is the evidence. Look at the order in which things got fixed. Management structure was fixed in a quarter, and boAt did exactly that. Capital structure was fixed with money, and OYO is using ₹4,987 crore of fresh proceeds to do it. Profitability was fixed over four to eight quarters of operating discipline, and the refund and attrition numbers show what that actually looks like. Governance, litigation and control environment were not fixed at all. They were disclosed. That is the whole distinction. A company can buy its way out of a balance sheet problem and hire its way out of a management problem. It cannot do either with a control environment, because the evidence a regulator and an investor want is a multi year record of the controls having operated, and you cannot create that record after the fact. You can only start it earlier. Which means the founding decisions about how your data, consent, audit trails and disclosures are governed are, functionally, listing decisions. They are just being made five to seven years before anybody calls them that.

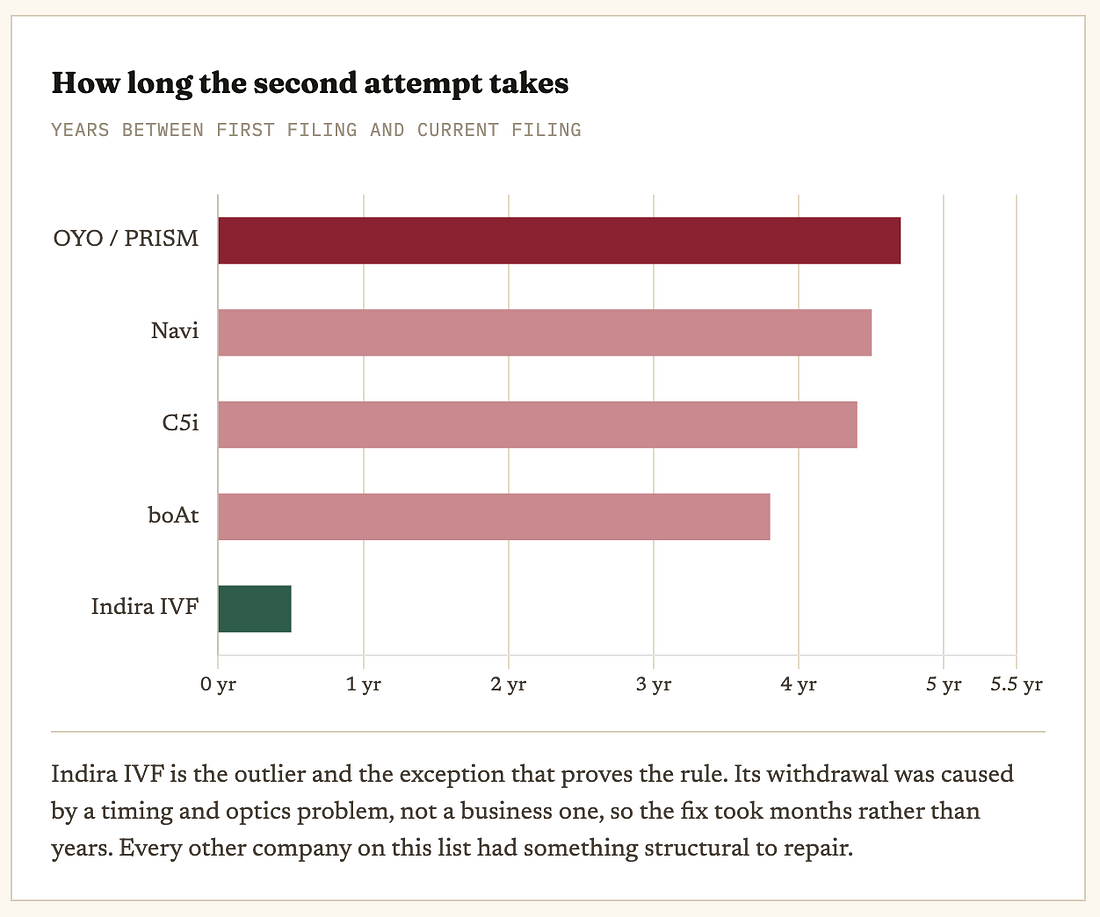

Read the two ends of that table against each other. The top half is a timing problem. You wait, you raise, you reorganise, and you file again. The bottom half is not a timing problem at all. It is a record keeping problem, and a record cannot be backdated. Which is why the cohort clusters where it does. Nobody in this list took five years because the market stayed shut for five years. The market reopened repeatedly across that period. They took five years because the things they needed to fix were the things that only resolve on their own schedule. The two minute testWhen a company files again, ignore the issue size. Look at how much the insiders are selling in attempt two compared with attempt one. If they are selling more, the company waited for the market to change. If they are selling less, something inside the company changed. It is not a verdict and it is not always damning, but it is the fastest signal available in a document that runs to several hundred pages, and it is on the cover page of every DRHP. OYO went from roughly 17% offer for sale to zero. Meesho cut its offer for sale by 40% before listing. boAt’s founders doubled their personal sale on a smaller issue. Run the test, then go looking for the reason. The trilogy that started three issues ago asked why the exit door had narrowed, then what a listable company actually looks like, and now what happens to the companies that reach the door and turn around. The honest answer across all three is that the listing is a lagging indicator. By the time a company is at the filing stage, most of what determines the outcome was decided years earlier, in decisions nobody labelled as IPO decisions at the time. The second attempt is where that becomes visible. Everything a company could fix quickly, it fixed. Everything still in the document after five years is there because it could not be. A note on the numbers.IPO figures move fast and several of these are live. OYO’s final prospectus, price band and valuation were not confirmed at the time of writing, and reported valuation figures for its 2021 filing vary across sources between roughly $9 billion and $12 billion. Issue structures for confidential filings, including C5i and Indira IVF, are not public. Every figure here should be re-verified at source before it is quoted. Thanks for reading. If you know a founder who is two years from a filing and does not think of it that way yet, this is the issue to send them. Shubham Bopche - Editor Venture Unlocked is free today. But if you enjoyed this post, you can tell Venture Unlocked that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

Saturday, 18 July 2026

The Second Attempt

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment